Market Snapshot: August 2021

In summary

- COVID Delta variant has created widespread lockdown across South East Australia putting Australia into a mini-recession until vaccination levels are sufficiently high for re-opening. This trend has also occurred around the world where hospital systems are under threat due to specific unvaccinated populations.

- Vaccination is key to economic recovery but so too is the avoidance of a vaccine resistant COVID strain.

- Bond yields slowed their decline resulting in flat return from defensive assets.

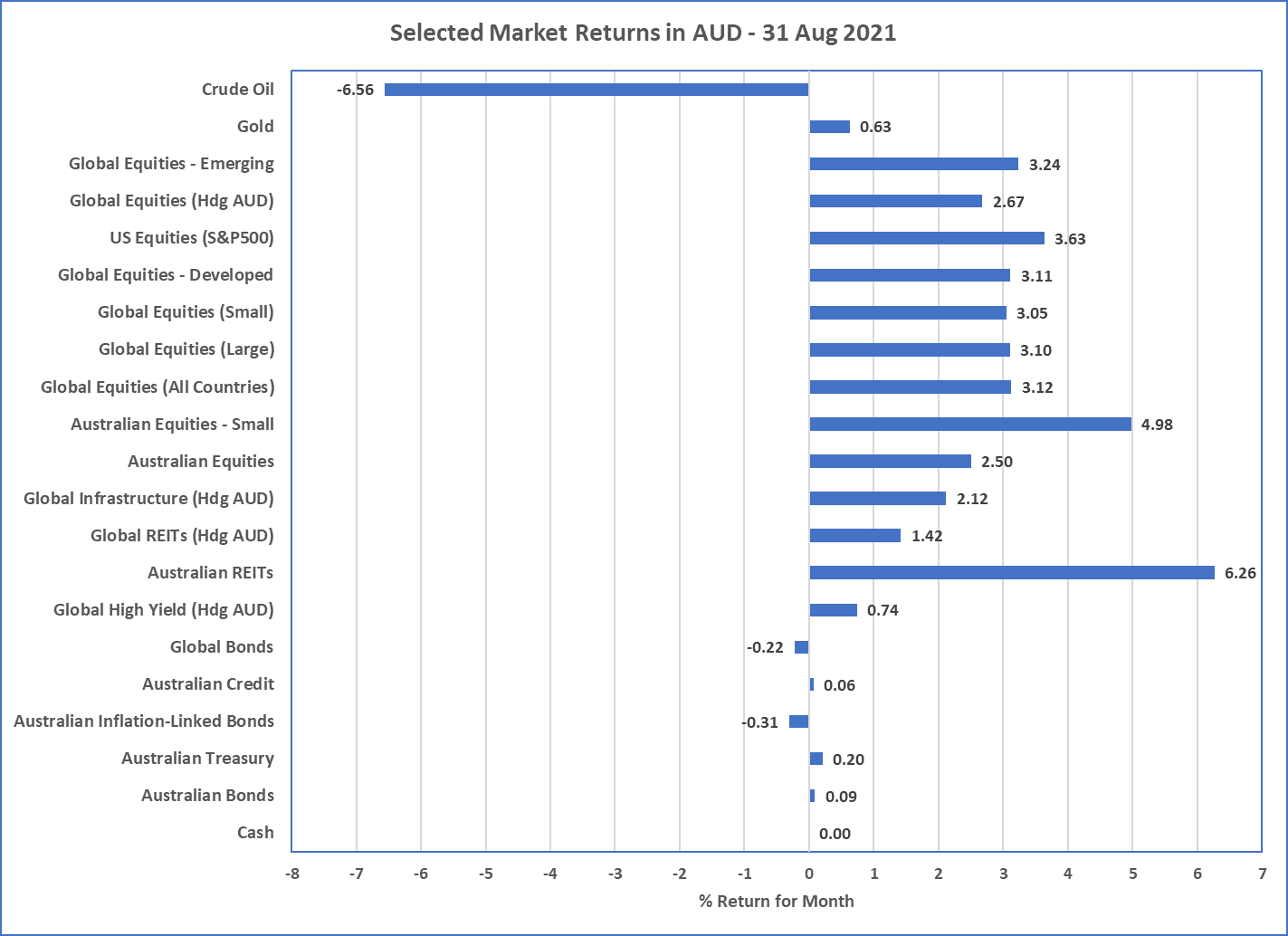

- Equity assets continued their strong return momentum which also continues record high valuations in various markets including USA. Valuation is a significant investment risk.

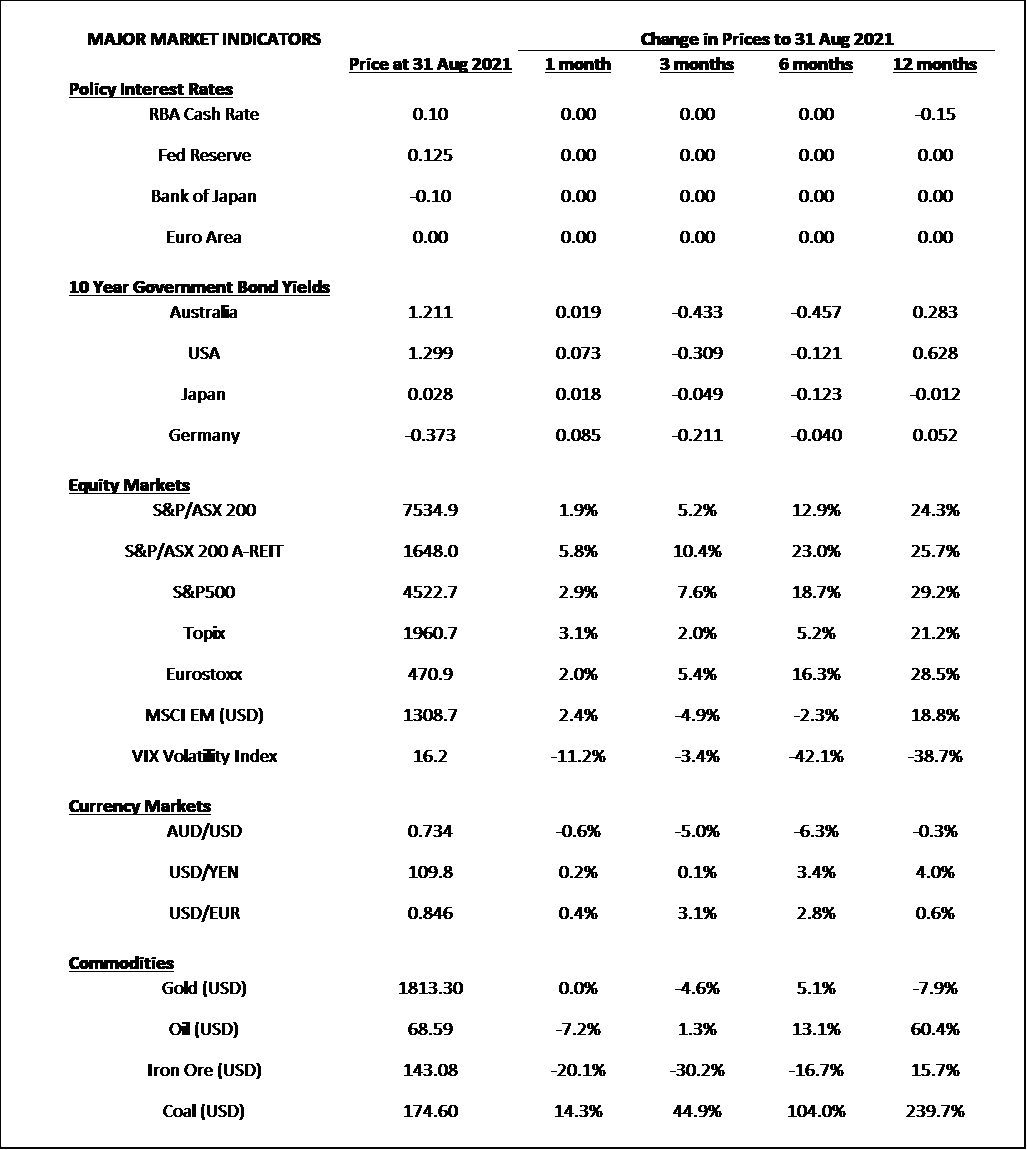

- Australia’s economy and currency have also weakened due to massive decline in Iron Ore prices (which were down over 20% in August alone).

- Our investment strategy continues its focus on diversification avoiding concentrated risks/bets. Whilst Cash and Bonds have low expected returns we carry small investment grade quality credit allocations to boost these returns and our concerns around equity valuations are tempered with defensive-like equity strategies.

Chart 1: Tough month for China and therefore Emerging Markets

Sources: Morningstar Direct

What happened in August?

Pandemic

Australia continues lockdown … may just miss recession.

- Whilst the June quarter’s GDP figures showed a higher than expected positive number, 0.7%, Australia is currently in a short recession thanks to the widespread COVID lockdowns across NSW and Victoria.

- These lockdowns have resulted in many workers temporarily out of work and with little government financial assistance, this lockdown will result in a significant negative GDP quarter for September.

- Both NSW and Victoria both admit their zero COVID policy is now a thing of the past as they focus on maximum vaccination as quickly as possible. The other states will likely continue their hard stance to avoid COVID spread as they also focus on maximum vaccination before the Australian economy opens up as a whole. A strong hospital system is a focus that COVID will always threaten.

- It appears COVID is here to stay and our pre-COVID normal economy appears unlikely to return as the world fights new strains of COVID and hopes vaccinations can continue to protect.

Markets

Bond Yields settle and Equities march on

- After strong yield reductions in recent months, August was a month of relative quiet as bonds settle down. This meant all Cash and Bond securities provided relatively flat returns for August.

- With Cash and Bonds providing little to no return potential the money flow during August into risky assets, like equities, continues. Strong positive returns were received for all.

- In terms of commodities, Gold was relatively steady during August whilst Australia’s number one export, Iron Ore, continued its massive decline, down over 20%. Oil also declined by around 7% providing some relief at the bowser thus helping the global economy’s back pocket and a little surplus spending money.

Economies

Bipolar global economy continues.

- The Delta variant continues to cause havoc around the world with another surge in cases creating lockdowns in the lowly vaccinated areas. Lockdowns will be needed to help local health systems but will inevitably create small economic shocks.

- Overall, the global economy is growing from its 2020 lows, currently relies on high vaccination rates, but what the Delta variant has shown is that COVID-19 is resilient, and the hope is that the vaccinations remain effective towards whatever the next variant brings.

Outlook

The risks and outlooks remain the same as last month insofar that the global economy will continue to grow as vaccinations increase and economies open and increase travel ability.

Risky markets also look riskier and riskier as valuations shoot for the sky. It is possible that this momentum will continue whilst the

economic outlook improves, and cash and bonds provide unattractive yields. But we continue to avoid too many concentrated bets and use

diversification and regular rebalancing to manage risks whilst maintaining allocation to growth.

Major Market Indicators

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL 491619