Market Snapshot: December 2020

In summary

- December was a much quieter month than November although most risky assets continued to perform well.

- Most weakness was in Australian dollar terms due to a weaker US Dollar. Rising bond yields also meant Australian bonds performed poorly.

- December commenced the rollout of some major vaccines creating some light at the end of the COVID tunnel. Unfortunately, COVID case and death rates are at record highs in most of Europe and the USA resulting in more lockdowns which are likely to impact short term economic growth.

- Portfolios continue to focus on diversification, avoiding concentrated bets, and regular rebalancing is likely to feature in a potential volatile 2021.

- All investors should expect low returns (i.e. low to mid-single digits % pa) from most asset classes over the next 5 to 10 years. Current valuations appear priced to perfection with an expectation of very strong economic growth for some years to come.

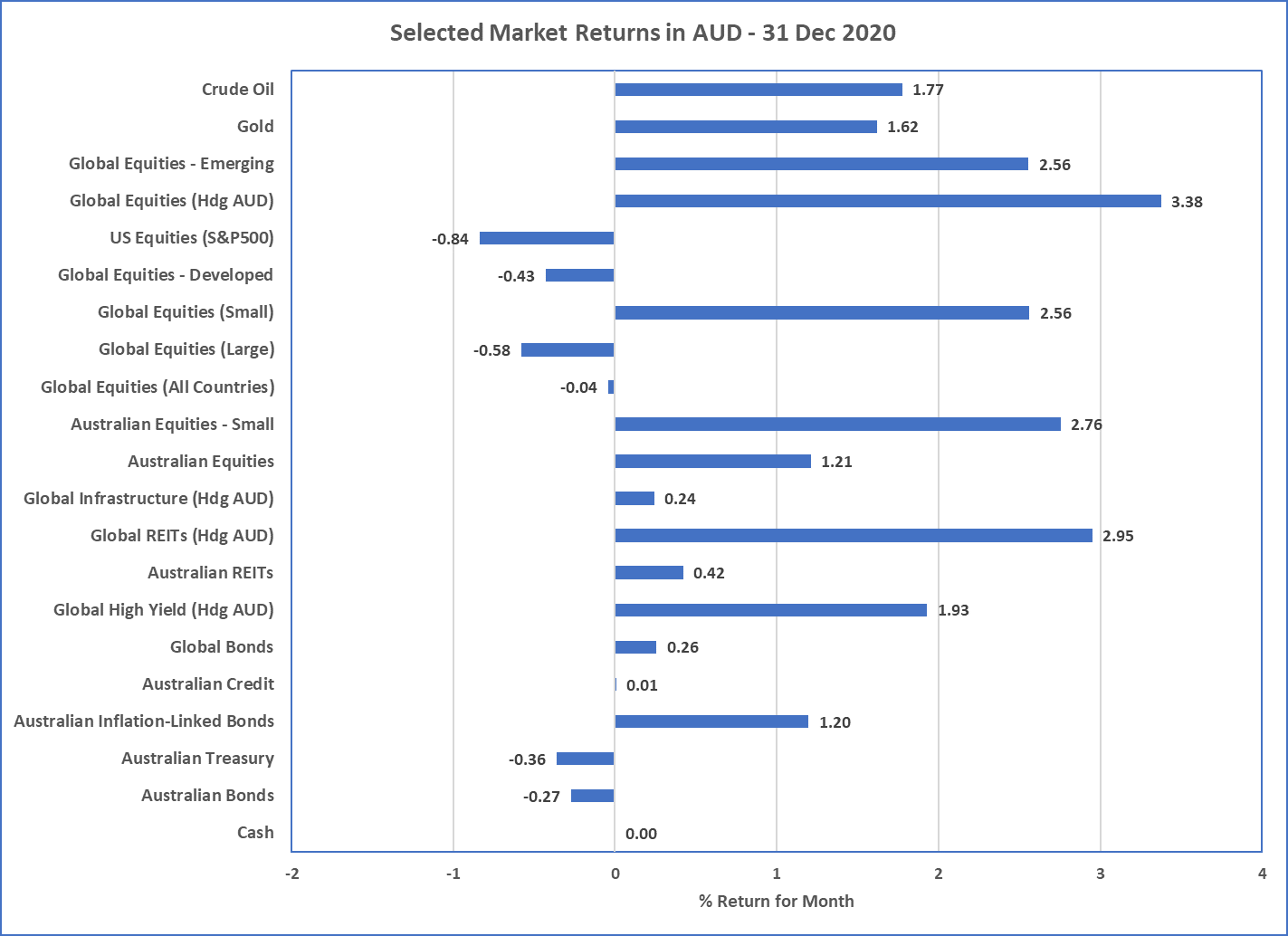

Chart 1: Markets produced mostly positive results across all asset classes

Sources: Morningstar Direct

What happened in December?

Pandemic

- Not unlike the rest of 2020, December was again all about COVID-19 but whilst record cases and deaths across Europe and USA dominated many headlines, so too did a broader global roll-out of the first vaccines with the strongest research results so far … Pfizer BioNtech, Moderna, and Astazeneca/Oxford University vaccines.

-

At least one of these vaccines has been approved for use in USA, Canada, UK, India, some Latin American countries, and much of Europe.

- The roll-out is moving slowly and it will take some time to see the effects but with record levels of deaths and new cases, these vaccines can’t come soon enough.

- Given Europe is locking down again and an increased chance of this happening in the USA once Joe Biden takes the presidential reigns, slow economic output over the final quarter of 2020 and first quarter of 2021 is likely.

- Mixed economic data is a strong likelihood during the first quarter of 2021, and it is highly likely this may result in higher volatility for equity markets as weak economic data battles with the positive potential of wider vaccination roll-out throughout the world.

Market Response

- The vaccine rollout is clearly a positive for the global economic recovery and risky markets (such as equities, commodities, and property) generally responded positively.

- In local currency terms, Developed and Emerging Market equities were up between 2.5% and 3.5%, whilst Australian equities were up a little over 1%.

- High Yield gained almost 2% as credit spreads continue to tighten (in English this means the risk of loan defaults reduced), and Crude Oil gained almost 2% in Australian dollar terms and almost 7% in US Dollars.

- When risky markets are positive, it is common for the US Dollar to weaken as it is seen as a safe haven currency and during December it weakened against all major currencies including the Australian dollar which is now trading at a multi-year high of around $0.77 to $0.78USD.

- The weaker performing asset classes were the generally safer ones which included Australian Bonds (down 0.3%), and Cash (essentially 0).

- In context, after some massive returns in the month of November (e.g. Oil up ~20% and Equities more than 10%), December was a relatively benign month in terms of total returns.

- It is worth noting that the US Volatility Index, which often serves as a predictor of risk, was up around 10% during December suggesting some equity market insurance may have been purchased in anticipation of difficult markets ahead.

Valuations still high

- The continued bull market in risky assets also means that many more market commentators are talking about the high valuations and increased risks about a significant sell-off to readjust.

- Either way, high valuations mean a low return future unless economic growth sustains above average levels.

Geopolitics

US Election results … but markets appear unaffected

- From a geopolitical standpoint it appears Donald Trump is doing everything he can to overturn the election result and disrupt the inauguration of Joe Biden as the next President of the USA.

- Markets appeared to have taken little notice of this and it is unlikely to have any significant impact as he increases his rhetoric.

Georgia matters most

- The Georgia Senate run-off election is the more crucial event as it will determine how much opposition Joe Biden has to face to execute his policy agenda.

-

A Republican win will create some difficulty and will reduce the likelihood of future stimulus efforts whilst a Democrat win will provide

the opposite and therefore increase the chances of a faster economic recovery.

- This is simply due to the Republican’s general concerns about higher debt levels from fiscal stimulus whilst Democrats have a stronger alliance with Keynesian economics which encourages fiscal stimulus no matter what when economic times are tough.

- At the time of writing it appears the Democrats are set for the win.

Other Geopolitical Issues in the background

- For now, other geopolitical issues are largely in the background and unlikely to affect markets is any massive way. This includes USA-China relations, USA-Iran tensions, and BREXIT. For the most part, there is likely no new information or there is a wait for Joe Biden to start his term.

Outlook

- It’s still all about COVID-19, vaccines, lockdowns, and searching for a path to recovery.

- We don’t really know how long it will take so there are many unknown unknowns and portfolios continue to be focused on diversification without any concentrated bets.

- All asset class valuations appear expensive and those that appear cheaper (e.g. Global Property) carry the greatest risks (thanks to lockdowns, et al.).

- Market volatility is a likely feature during 2021 so risk management via diversification and consistent rebalancing are likely to be the dominant portfolio management features.

- It is possible that effective vaccines results in a fast return to normal and higher than expected inflation. But at this stage inflation is not expected so portfolios are not currently positioned for this but it is the one issue that is lurking in the background.

Overall, not a great deal has changed from November… Cash and Bond yields continue near zero in Australia and around the world and likely to stay there for some time; Australian and global equity markets continue at or near record high valuation levels as the global economy climbs very slowly out of the depths of recession.

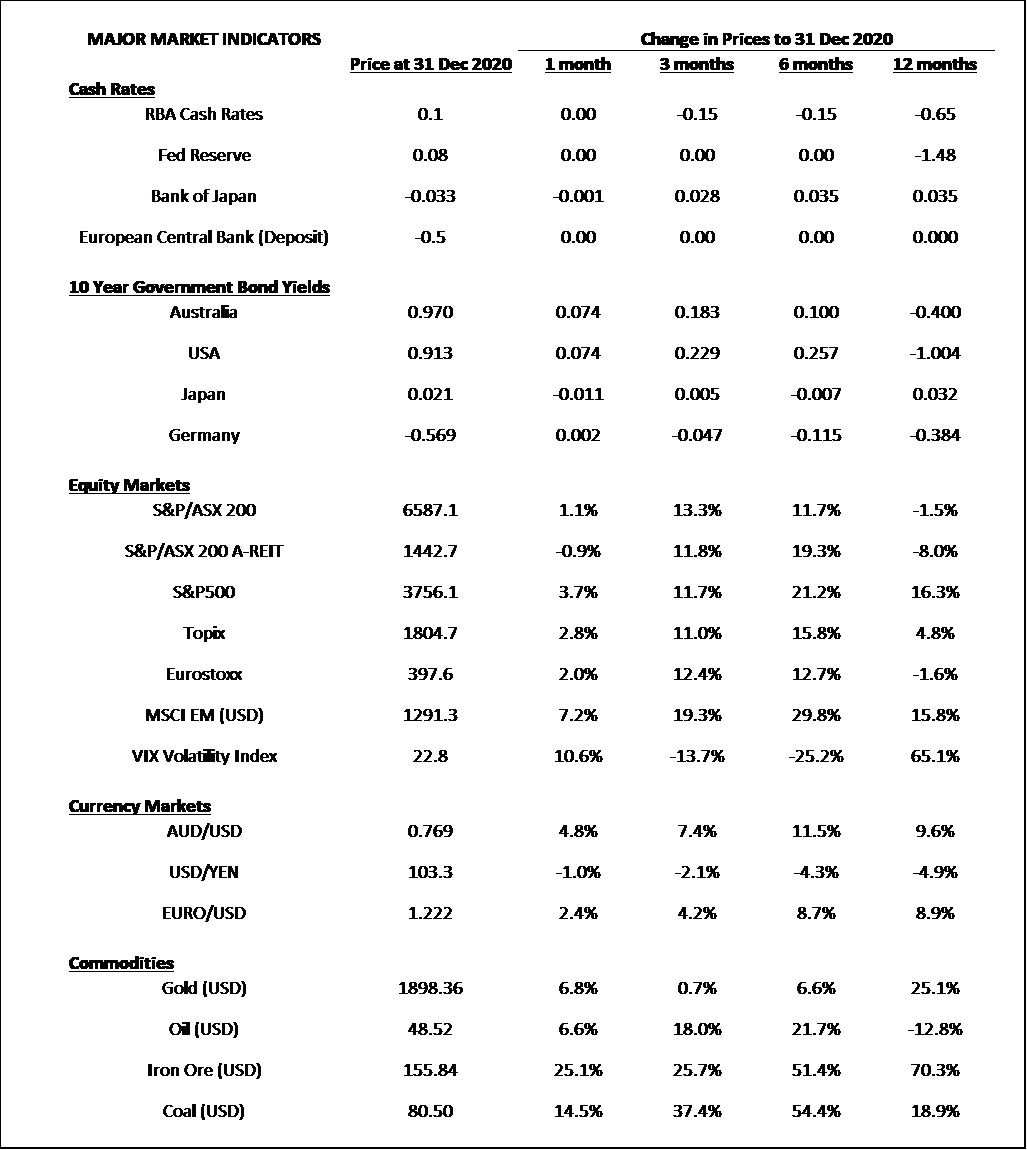

Major Market Indicators:

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL 491619