Market Snapshot: February 2021

In summary

February showed that Bonds aren’t always boring as longer-term interest rates increased substantially resulting in the biggest bond sell-off in Australia (& elsewhere) since 1994.

As a result, the usual defensive asset classes suffered negative returns in February (If Bond Yields go up, prices go down).

Equity markets were volatile although largely due to a shift from growth securities (like Technology) to the cheaper, Value-style securities (like Energy companies and Banks).

Higher bond yields are the market saying the economic outlook is stronger and inflation is likely to increase. That said, the central banks are still indicating they are likely to leave cash rates around zero for several years yet, suggesting they disagree that inflation is on the way.

The market’s positive outlook on the economy is off the back of the strong expectations of the various COVID-19 vaccines and that herd immunity is coming. Thanks to the vaccines and some lockdowns, February was a relatively good month as growth rates in COVID-19 Cases and Deaths have dropped around the world.

Looking ahead, market volatility is likely to continue as both bond markets and equity markets continue their repositioning for the improved outlook.

Our portfolios are well diversified but some interest rate sensitive assets (e.g. those exposed to Property) have expectedly underperformed. Value style equity strategies are poised to perform well whilst the portfolios are positioned appropriately with reduced exposure to these rising interest rates compared to market benchmarks.

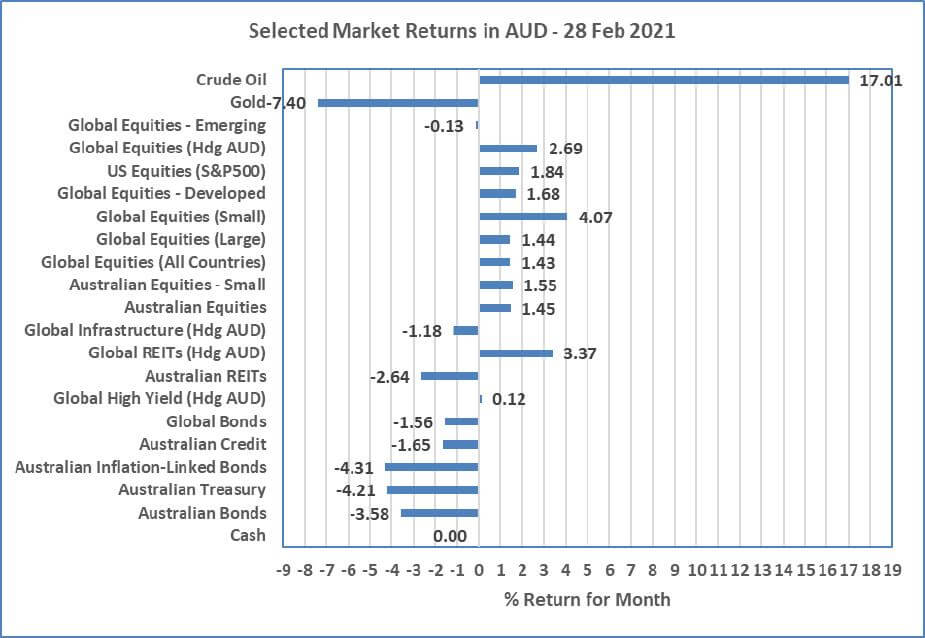

Chart 1: February markets were mostly positive for risky assets and not so defensive assets

Sources: Morningstar Direct

What happened in February?

Pandemic

Finally, reduction in case and death rates across the world

-

The global vaccination is now well and truly underway and along with various lockdowns, global case numbers and death rates have

substantially reduced.

- Tragically, the USA continues to be the worst country in terms of total numbers. It recently passed 500,000 deaths and still averages more than 2,000 deaths per day but has fully vaccinated around 10% of the population which is helping significantly.

- Australia and New Zealand continue to lead the world with their eradication policies, and a few recent short lockdowns in both countries appeared to have been effective without massive economic disruption.

- Recovery from the Pandemic continues to be the number one issue for economic growth over the next few years. So far so good, but there is still a long way to go before borders re-open and the global economy is back to normal.

Markets

Bonds … not too boring at the moment

-

Whilst January demonstrated some unique risks of short selling via Gamestop, February has shown that Bonds aren’t always boring with

significant steepening of the Yield Curves across Australia, New Zealand, USA, and more. In English, this means longer term to maturity

Bonds had sharp interest rate increases, which also means their prices fell quickly.

- Chart 1 demonstrates this with negative returns from Australian Treasury, Australian Inflation-Linked Bonds, and Australian Bonds, and to a lesser degree Global Bonds.

- These higher interest rates also mean that interest rates sensitive securities came under pressure and is the primary reason for the decline in Australian REITs and Global Infrastructure. Global REITs have not yet recovered as quickly as these other two asset classes, so were probably less sensitive to rate increases (for now).

-

Chart 1 also shows generally positive returns across equity markets although there has been some volatility with many days experiencing

greater than 1% moves.

- High interest rates should place equities under some pressure as, in theory, it means equity market valuations should decrease.

- The last month has seen a sell-off of the expensive growth stocks in favour of the cheaper value stocks (which also includes energy stocks that have been supported by the strong rise in Oil …. See chart 1).

Geopolitics

All quiet on the western front

Whilst there is always plenty happening around the world, there is nothing substantial affecting markets at this point in time. US-China

and Australia-China relations will be a major theme but all is relatively quiet for now.

Outlook

-

Higher bond yields are the markets way of saying that higher inflation from strong economic growth is coming. At this point in time, it

appears the Central Banks don’t believe it and they (whether Australia, USA, Europe, etc.) have stated they will keep cash rates low for a

number of years. In Australia’s case, that is until 2024.

- Who will be right? … obviously time will tell, but recent academic research has shown that during a recession or depressed economy, monetary and/or fiscal stimulus is instantaneously inflationary but because it is offsetting a deflationary recessionary environment, the outcome is still a low inflation one.

- Bond yields are approaching a point where they may be meaningful again and therefore may results in shifts away from riskier assets or at least higher volatility (the latter appears to be taking place now).

- Either way, the market is certainly confident the vaccines will do what they are supposed to do and herd immunity from COVID-19 is closer than we may expect. This is great news for the global economy and recent strong numbers are expected to continue in 2021 (please note, we are still at 2019 GDP levels so are still at a low base).

- This may, in turn, provide confidence for equities and risky assets, but they continue to appear relatively expensive especially USA) and the current rotation from high growth companies to the recovery story has some time to play out yet (if it does).

-

Overall, the outlook is currently a volatile one as the battle plays out between bonds and equities. Bond yields increase by a lot and

equity valuations must decrease.

- Our portfolios are diversified and avoiding concentrated positions.

- Our portfolio’s defensive allocation, are underweighted to rising interest rate risks which is somewhat helpful in this environment (returns will still be subdued).

- Our portfolio’s equity allocation is well diversified across various styles including Value style which appear to be benefiting from recent market movements. Particularly since the vaccines suggested a return to a normal economy is possible.

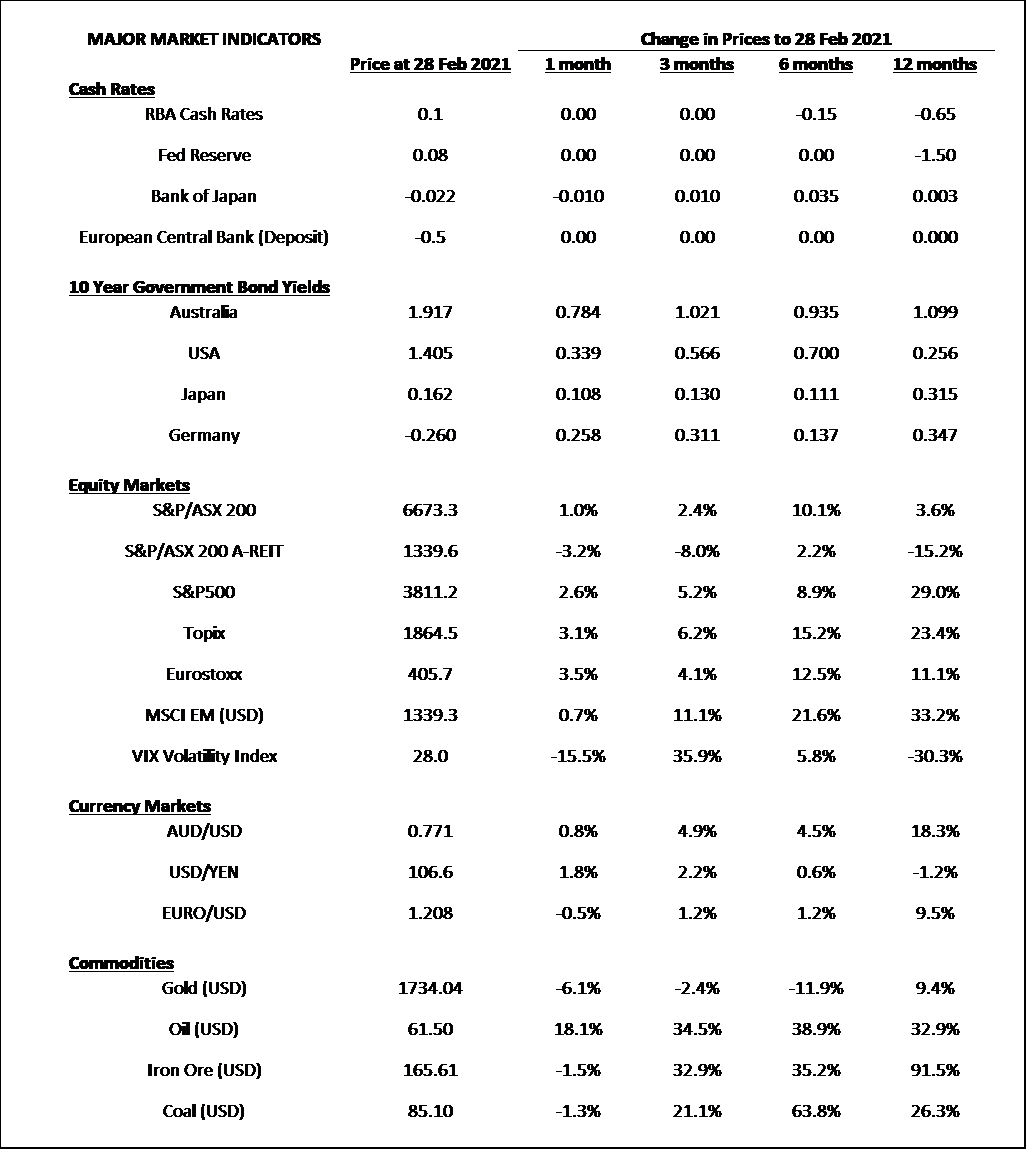

Major Market Indicators

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL 491619