Market Snapshot: February 2022

In summary

- The geopolitical risks of a Russian invasion has come to the fore resulting in more price hikes for energy, declines in equity markets accompanied by high daily volatility. Whilst this war continues, these trends are likely to continue so a resolution is required before these trends will likely change.

- Inflation has hit another multi-decade high in the USA, increasing the likelihood for the Federal Reserve to increase their case rates. This will likely put upwards pressure on bond yields, but the current geopolitical tensions could reduce both of one of these scenarios.

- Australian inflation is surprisingly low, despite high energy, and after a low-ish wage inflation result during February this means the Reserve Bank of Australia is unlikely to increase its cash rate in the short term (although they have stopped their bond buying program).

-

Preferences in portfolios are shorter duration, as bond yields and cash rates appear more likely to increase than decrease in the long term;

combination of defensive and lower valued securities in equity markets, as inflation will likely favour lower valuation securities and lower

volatility securities provide some levels of protection in these volatile markets.

- Diversification and regular rebalancing when portfolios significantly differ to strategic weights are prudent approaches to investing in today’s scary times.

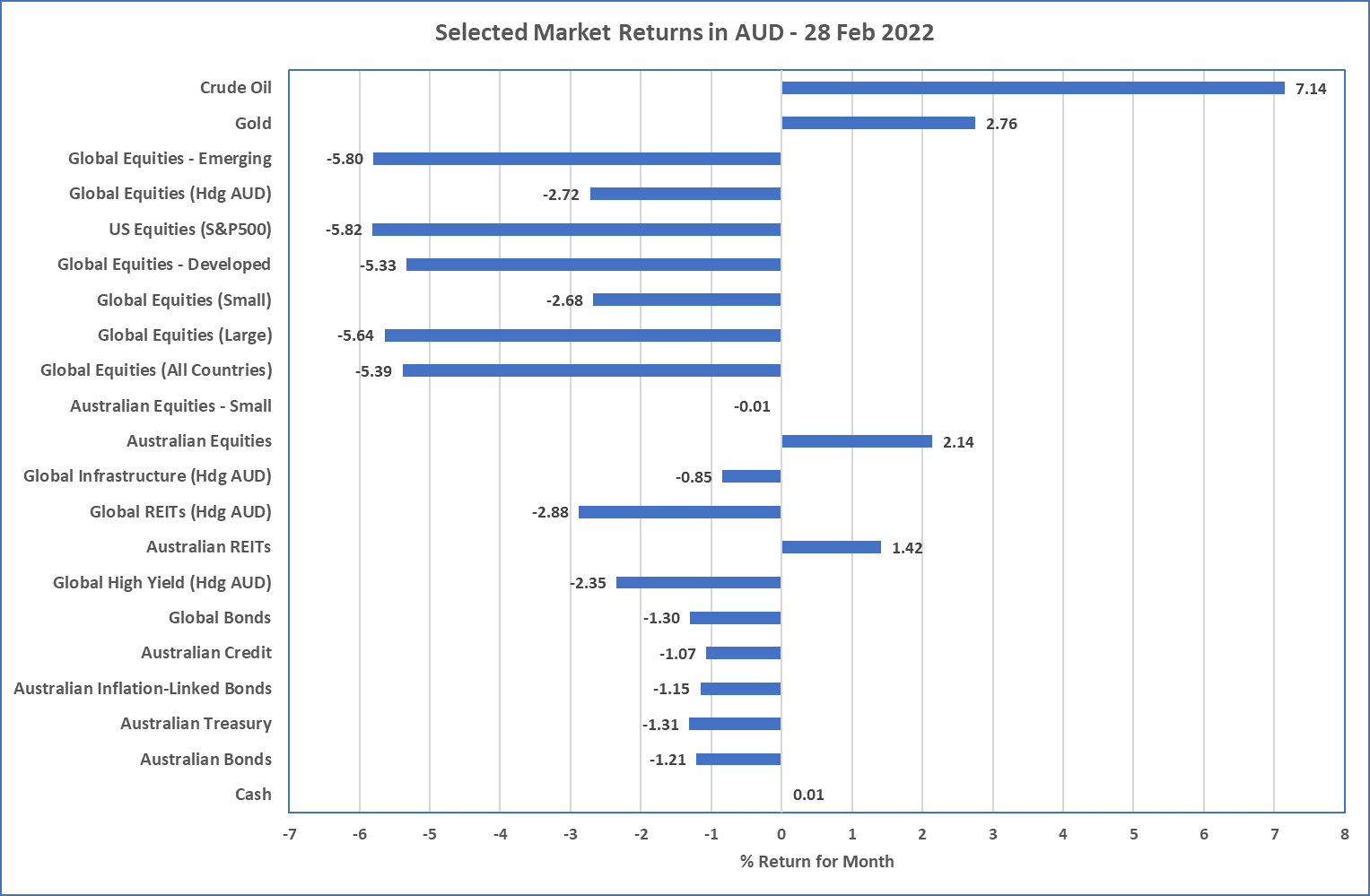

Chart 1: Another difficult month in traditional asset classes

Sources: Morningstar

What happened in December?

Pandemic

A slightly fading risk

-

Whilst Omicron is in decline in Australia and the newspaper headlines have shifted elsewhere, it is still producing the highest case and

death rates since the Pandemic began. This is due to Omicron’s two variants being significantly more contagious than previous strains such

as Delta.

- That said, it does appear that the vaccines are mostly effective, and there is still light at the end of this tunnel as case and death rates are declining.

- The major risk continues to be a vaccine-resistant variant and there are plenty of unvaccinated to assist this creation.

Markets

Geopolitical risk to the fore

- Last month we mentioned that the potential for a Russian invasion of Ukraine was placing upward pressure on energy prices, and this has continued as Oil and Coal (see table) produced big double digit returns for February whilst most equity and bond markets went negative.

- February was the second month in a row where traditional assets were mostly negative but the one exception was the Australian market, where the S&P/ASX 200 increased by oer 2%. This was ably supported by the sometimes inflation-hedge, S&P/ASX 200 A-REIT index (otherwise known as listed property securities).

- Emerging markets dropped almost 6%, which is unsurprising considering Russia’s starting 12% allocation (which is now zero as the index has removed Russian exposure like many fund managers).

- Global developed markets also declined over 5% and this was led by the continued expensive US, S&P500 (down almost 6%).

- Bond yields across most markets increased as inflation fears continued, and this resulted in declines between 1% and 2.5% across Australian and global bond markets.

- The Australian dollar increased a little against the US Dollar which is somewhat contrary to usual behaviour as declines in risky markets usually see a strengthening US Dollar as funds shift to its safe haven status.

Economies

Inflation still the major theme

-

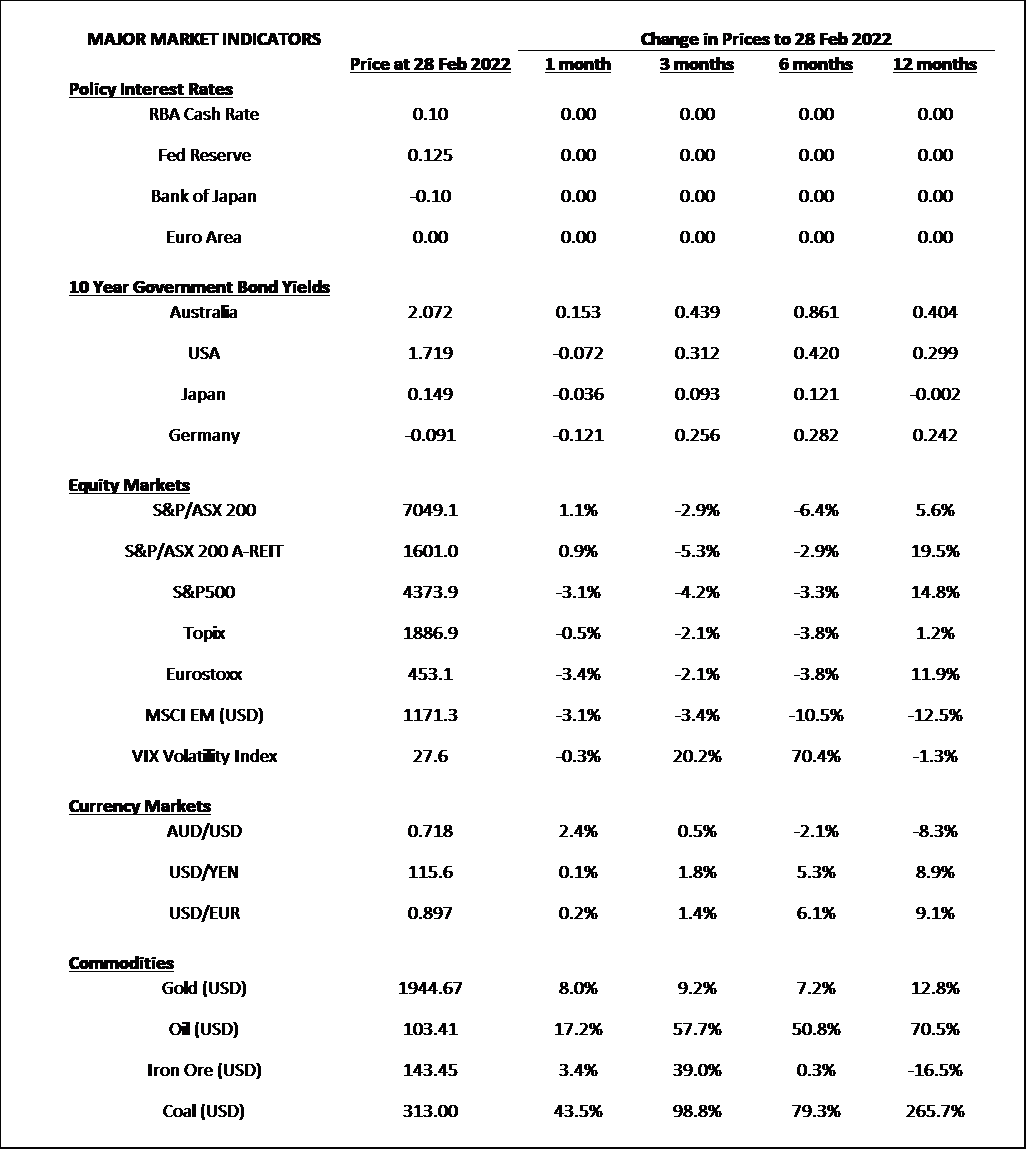

Latest inflation figures from USA continued to be at multi-decade highs and the end of January annualised inflation is now 7.5%.

- This high level, combined with expectations of sustained higher inflation (led by high energy prices) has resulted in expectations that they Federal Reserve will raise rates around 5 times during 2022. The one caveat may be how it factors in the risks of Russia / Ukraine war.

- As mentioned last month, Australia’s underlying inflation is now at its highest level since 2014 (2.7%) but with a somewhat benign wage inflation result announced during February (2.2%), it seems unlikely the Reserve Bank will follow the Federal Reserve, and Australian cash rates are likely to stay at their record lows for a few months yet.

Outlook

-

The Russian invasion of Ukraine will likely keep energy prices very high over the short term and this will likely lead to higher prices

given energy is a major input to everything.

- Higher prices mean higher inflation, and this ultimately leads to higher cash rates and bond yields suggesting portfolio’s current bias to shorter duration continued to be preferred.

- High global inflation and the increased geopolitical tensions also suggests equity markets will continue to be volatile over the short term. This also means diversification is key and the avoidance of concentrated bets is prudent as there are increased chances of market surprises.

Major Market Indicators

Sources: Tradingview, Morningstar, Trading Economics, Reserve Bank of Australia

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL 491619