Market Snapshot: January 2021

In summary:

- January was a challenging month as many markets paused after a very strong recovery from the COVID-19 induced March low. The exception being Emerging Markets, Global Smaller Companies (both up around 3%) and commodities such as Coal, Oil, and Iron Ore (up between 7 and 8%)

- Unfortunately, January was a terrible month for COVID-19 around the world with more than 100,000 total deaths in the UK and more than 400,000 in USA. Thankfully, the new vaccines are being rolled out around the world and this is expected to significantly slow the number of new cases over the coming months.

- January also saw Joe Biden inaugurated as the new President of the United States, but tragically also saw Donald Trump try to overturn the election result, allegedly contribute to a riot on the Capitol Building resulting in impeachment for the second time. Incredibly, Markets appeared unaffected by these events (I guess they predicted the outcome).

- Cash and Bond yields remain very low although January did see longer term yields increase slightly which is a positive sign for the longer term economic outlook.

- Equity markets continue to be in potential bubble territory as current valuations have rarely been this high in history (although neither has the amount of Fiscal and Monetary stimulus).

- All of that said, portfolios remain cautiously positioned and are widely diversified. They are slightly underweight growth assets, but carrying a generally overweight position to credit securities compared to traditional bond indices.

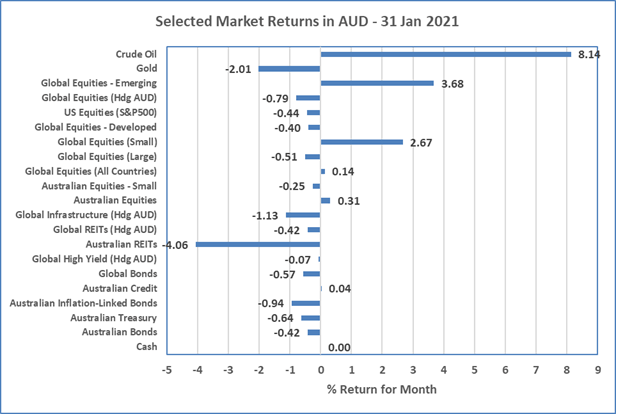

Chart 1: Markets produced mostly positive results across all asset classes

Sources: Morningstar Direct

What happened in January?

Pandemic

- Despite new vaccines being rolled out around the world at record levels, the Pandemic continues at horrible levels. USA have more than 400,000 deaths, UK more than 100,000 deaths and lockdowns increased instead of decreased to stop the rampage of more contagious COVID-19 variants.

- On the positive, new vaccines continue to show strong efficacy but time will tell whether they are effective to mutated versions of the virus.

- In Australia there were small outbreaks and lockdowns in Brisbane and Sydney but at the time of writing, Australia is very well positioned. Stricter rules around flying into Australia will hopefully be effective in keeping COVID-19 cases at low levels, but unfortunately will ensure economic growth remains contained.

Markets

A pause in January, whilst David takes out a Goliath or two

- After a very strong final quarter of 2020, most markets paused during January. The exceptions being Global Small Companies and Emerging Markets (both up around 3%), Energy commodities such as Oil and Coal (both up ~7%), and Iron Ore (up ~8%).

- The weakest performing major asset class, was Australian REITs (down ~4%).

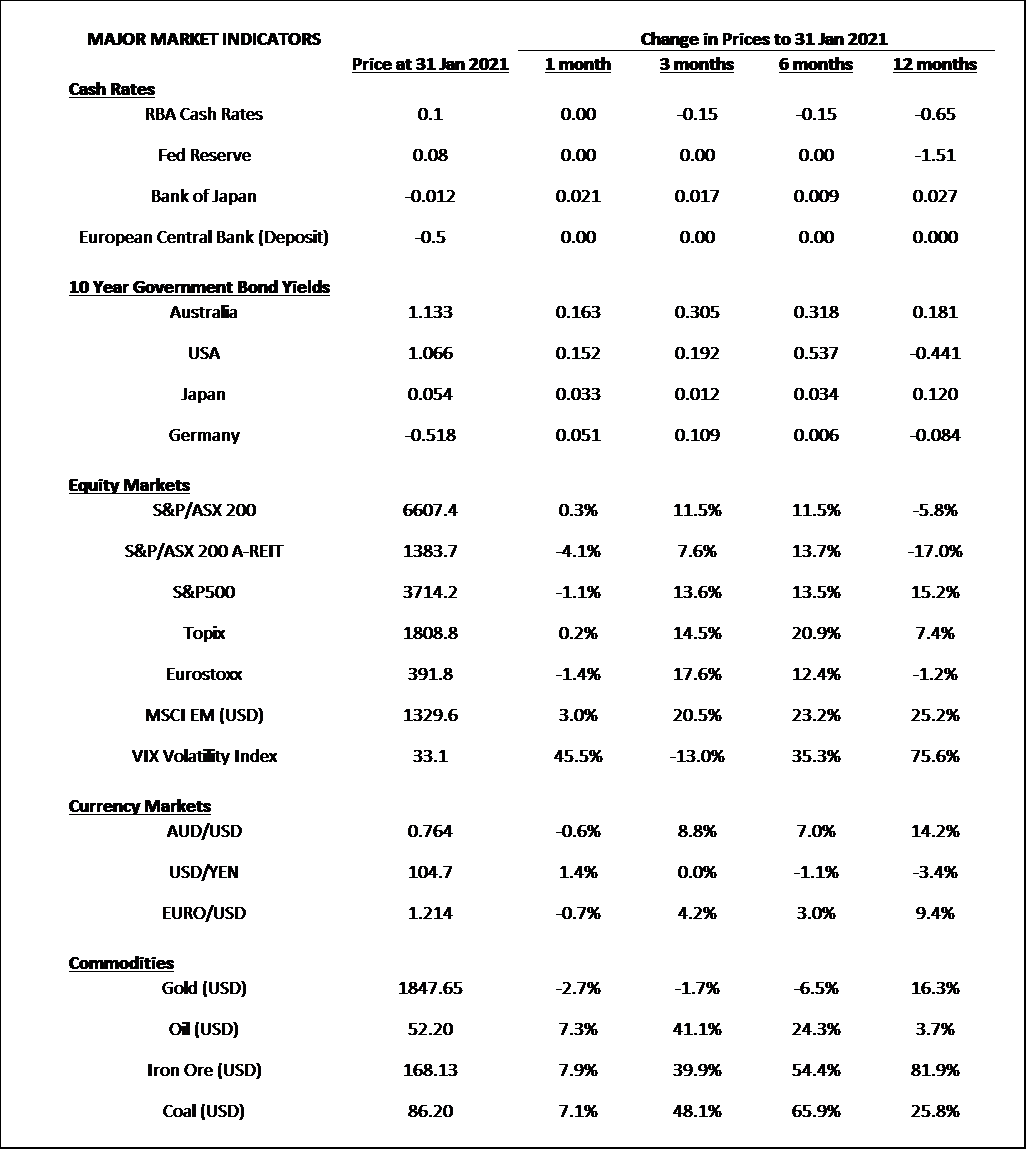

- Bond yields started to rise around the world and locally with the Australian and US 10-year bond yields training around yields of 1.1%. Whilst this does not sound like much, they are increases of around 15bps, which is quite significant for bonds and is generally interpreted as a positive sign for the long-term outlook for the global economy (but is bad for REITs)

- The Reserve Bank did not meet during January so all was relatively quiet in terms of Australian short term interest rates.

- The most interesting development during January was the trading in the struggling US company, Gamestop. Small investors from the social media platform, Reddit, appeared to have bought enough Gamestop stock to force many hedge funds to buy stock and close their “short” positions in the stock; only for the price to snowball upwards and force more purchases. This resulted in a few hedge funds losing several billion dollars from the actions of these retail investors/speculators. The SEC is now investigating for fraud as they try to find the people behind what appears to be illegal market manipulation. Either way, it is a warning to hedge funds of the dangers of shorting stocks (i.e. borrowing stock to sell in the hope it can be purchased later at a lower price).

Geopolitics

Democracy threatened … but markets barely noticed

- The events of 6 January will go down in history for the unfortunate reasons, as it was a day where US democracy was under threat and ultimately lead to the second impeachment of US President, Donald Trump. Thousands of Trump supporters stormed the Capitol Building, where Congress were about to confirm Joe Biden’s Electoral College vote win. The objective of the raid was to overturn the election and ultimately 5 people were killed including one police officer and a woman was show inside the Capitol.

- Whilst the rioters tried to overturn the election results, the S&P500 actually went up on 6 and 7 January … so no concerns on Wall Street whatsoever.

Outlook

-

As commentators increased their rhetoric about a sharemarket bubble, markets continued to be buoyed by the monetary and fiscal stimulus.

- Biden has announced a new $1.9trillion fiscal package and that is likely to provide short term momentum but there is no doubt that sharemarket valuation levels are high and in rare territory.

-

This adds up to potential heightened levels of sharemarket volatility and is reflected in the VIX index which at the end of January stands

at a fairly high value of 33.

- Portfolios are prudently positioned and are slightly underweight to growth assets with strategies that are designed to reduce downside risk. In addition, wide diversification without concentrated positions is an additional feature.

-

Whilst cash and bond yields remain near zero and likely to stay there for a long time yet (or until COVID-19 is behind us), central banks

and governments appear determined to avoid corporate collapses.

- Portfolios retain a slightly higher allocation to corporate debt compared to low yielding benchmarks.

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL 491619