Market Snapshot: July 2023

In summary

A good month for all asset classes

- Economic data in the USA and Australia both appear on the right track as inflation is reducing whilst unemployment stays low. That said, there continues to be contrary negative leading indicators such as negative bond yield curves suggesting weak to negative economic growth.

- Emerging Markets was the best performing equity asset class in July and this was despite China’s economic data showing near deflation as it’s inflation numbers are the opposite of ours and sits at 0. Deflation is often contractionary as people stop spending.

- US sharemarkets maintain their strength and higher valuations over the rest of the world. And this still presents as one of the bigger sharemarket risks as high valuations in the face of high cash rates appears somewhat incongruent as liquidity continues to be removed from markets.

-

With economies expected to slow and US sharemarket valuations at above average levels, caution continues to be the appropriate course

of action for portfolios. We continue to have comfort in Cash and High-Quality Bonds and prefer the cheaper sharemarkets including

Emerging Markets and Australia, over expensive USA tech.

- Global Small companies also appears attractively valued as their 2023 recovery isn't quite the same as the US Tech stocks, so if recession is avoided their potential is high.

- Overall, we maintain our preference for Diversification over concentration given the many divergent market signals.

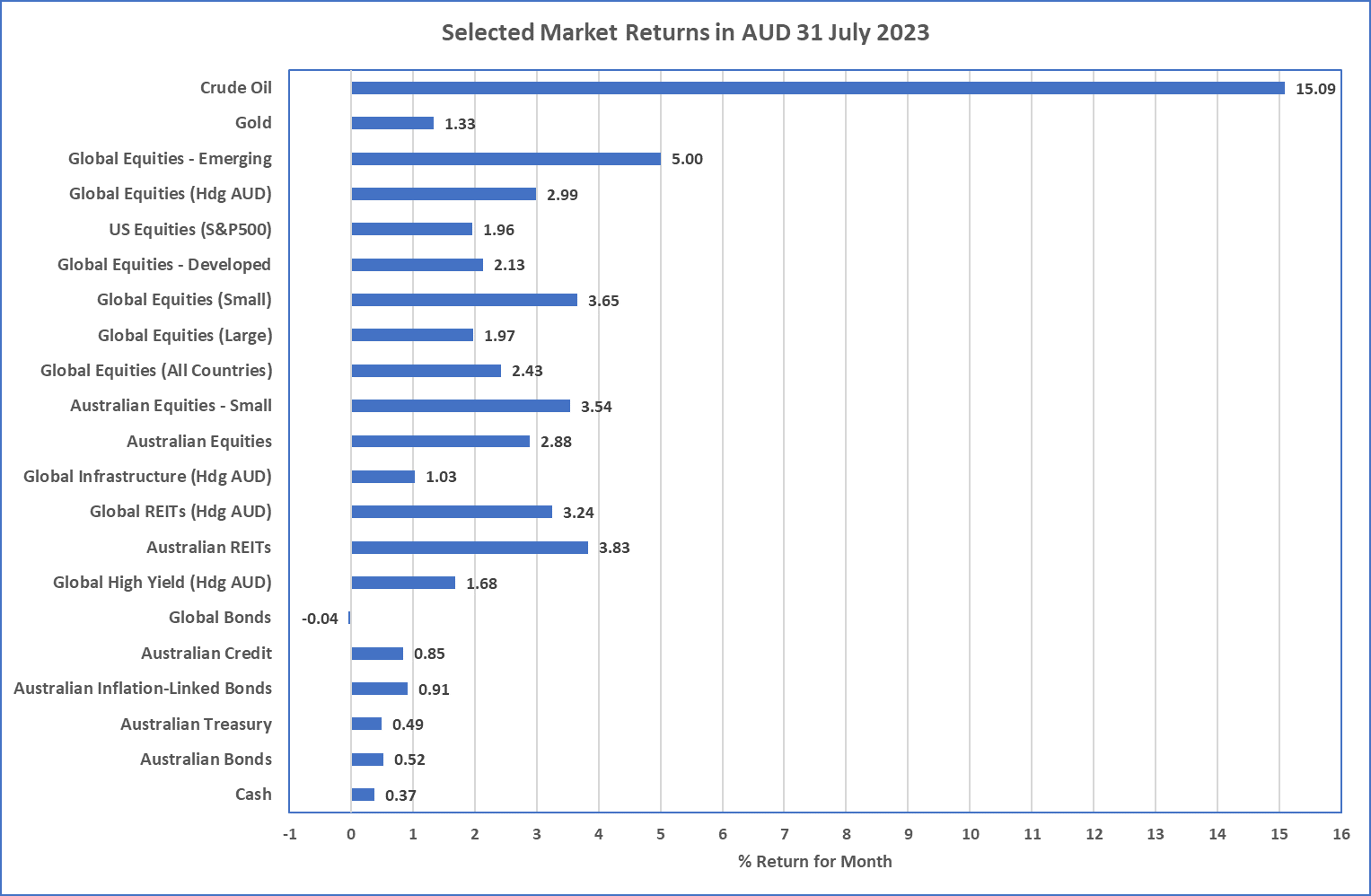

Chart 1: Everything looks great???

Source: Morningstar

What happened last month?

Markets & Economy

BAU

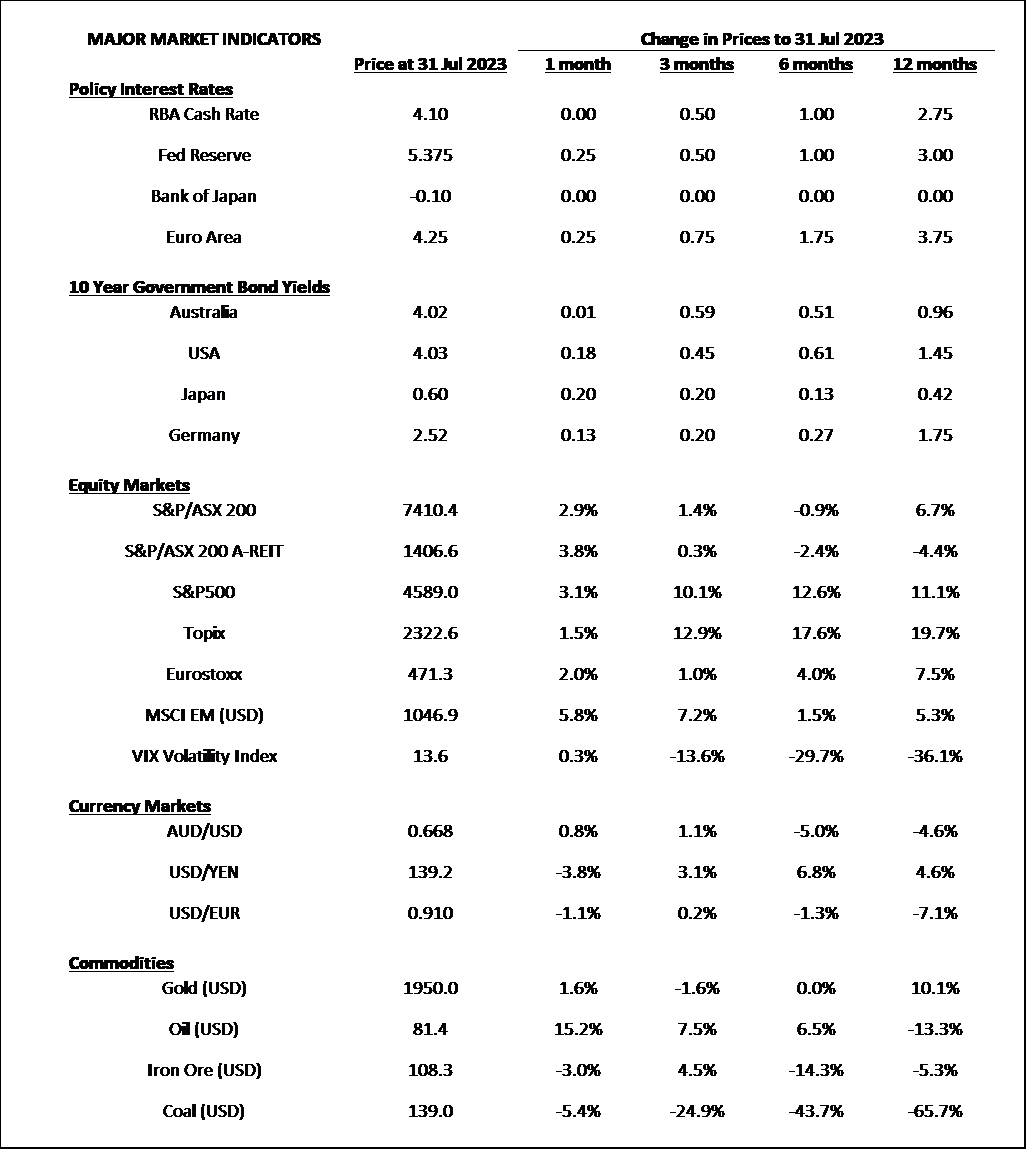

- USA inflation is now at 3%, unemployment somewhat steady and very low at 3.5%, and the June GDP increased quarter on quarter by a strong 2.4%. So the US economy continues to deny many leading economists suggesting there will be no recession. That said, this strength will provide the Federal Reserve impetus to further increase interest rates, and they increased another 25bps in July, to ensure the downward trend of inflation continues. Once again, this begs the question, will they go too far? Rates are currently at 5.25% to 5.5% and well above the 3% recent inflation so will it lead to contraction?

- This US economic strength was supported by strong returns by risky assets, as sharemarkets around the world returned between 2% (Developed Markets) and 5% (Emerging Markets), and Global High Yield returned a relatively strong 1.7% for July.

- In Australia, the RBA paused in July and August, despite inflation coming in at a still too high 6% for the June quarter. The Bond yield curve continues to be flat to negative suggesting a weak economy is before us as there is no additional premium for holding longer term bonds.

- Europe and China are the current global economic laggards. Europe is experiencing high inflation (~6.4%), contracting economies, whilst China’s inflation rate is teetering on deflation (i.e. it is 0%) and this is despite re-opening post-COVID inside the last 12 months. Some economists are suggesting that China may become the next Japan considering it’s declining and ageing population. Either way, China does present unique risks to global markets, including overspending on infrastructure, and bankruptcy amongst property developers, that cannot be ignored.

Outlook

The message remains unchanged …

- There is some comfort in the recent stronger than expected economic data including lower US inflation. However, rising central bank interest rates in the USA have resulted in recession 11 out of the last 14 times. If there is recession it has probably likely late 2023/early 2024. Caution remains as rates at 5.5% must have a negative impact on household and company balance sheets and net cashflow.

- Sharemarkets in the USA are still appear expensive with strong returns mostly coming from the large cap tech sector. This also results in risky asset caution, continued need for diversification, and extreme focus to avoid the disease of FOMO (fear of missing out). The darling of the recent boom is Nvidia whose numbers appear difficult to rationalise and are surely nothing more than speculation, despite the AI revolution we are likely entering.

- Long term bond markets are providing yields similar to Australian cash rates. So, our current preference is for diversification across different terms to maturity and are comfortable with longer duration as it will likely cushion equity market risks. We believe upward pressure on Cash rates still exists, so Cash is still the current King.

- As stated in previous updates, it is essential for all portfolios to diversify across asset classes and securities with a focus on the long term. It’s been an incredibly strong 2023 for global equity returns, particularly USA growth, but current valuations suggest this is highly unlikely to continue.

Major Market Indicators

Sources: Tradingview, Morningstar, Trading Economics, Reserve Bank of Australia

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL 491619