Market Snapshot: June 2025

Summary:

Geopolitical issues continue, all markets up … except gold

- Whilst geopolitics continued to dominate the news, it wasn’t tariffs this time as Trump’s Big Beautiful Budget Bill (the biggest ever transfer of wealth from poor to rich) passed through Congress whilst the US bombed Iran’s nuclear facilities to end the 12-day war between Iran and Israel. The war resulted in Oil prices increasing over 7%, whilst the budget bill further weakened the US dollar.

- Despite the geopolitical issues, most investment markets continued to produce strong returns in June. There are some tariff headwinds that may re-commence in July but markets tend to think the TACO (Trump Always Chickens Out) trade is best and the S&P500 tested new highs along with other strong markets, including Emerging Markets (which increased over 4%).

- The only negative performance from our monitored asset classes came from Gold. This is consistent with Gold playing its continued role as a hedge to chaos and risk.

- Real Assets and Bond markets produced small positive returns as most cash rates and bond yields didn’t significantly change over June. In Australia, the Reserve Bank of Australia didn’t change its cash rate, but short term forward markets are pricing in a few more reductions and cash rates are expected to be around 3% by the end of 2025.

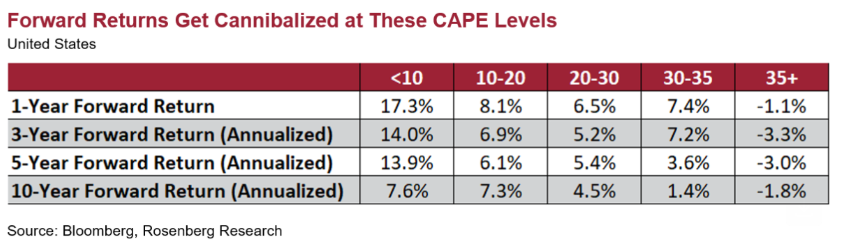

- Looking ahead whilst cash rates decline, we believe riskier markets will increase in volatility when tariffs are reignited over July and August and weaker global economic data is likely for the second half of 2025. As shown on pages 4 and 5 of this report, some of the USA valuations are very high and may influence a bearish outlook for many investors.

- Our core investment message today is to maintain diversification, focus on the long term, and regularly rebalance. Major risks continue to lie with expensive sharemarkets, including large companies of the USA, and we continue to favour quality (i.e. good profitability) and value (i.e. “cheap”) styles for long term investments in shares. Quality bonds are preferred as higher yielding below-investment grade bonds provide a historically low premium.

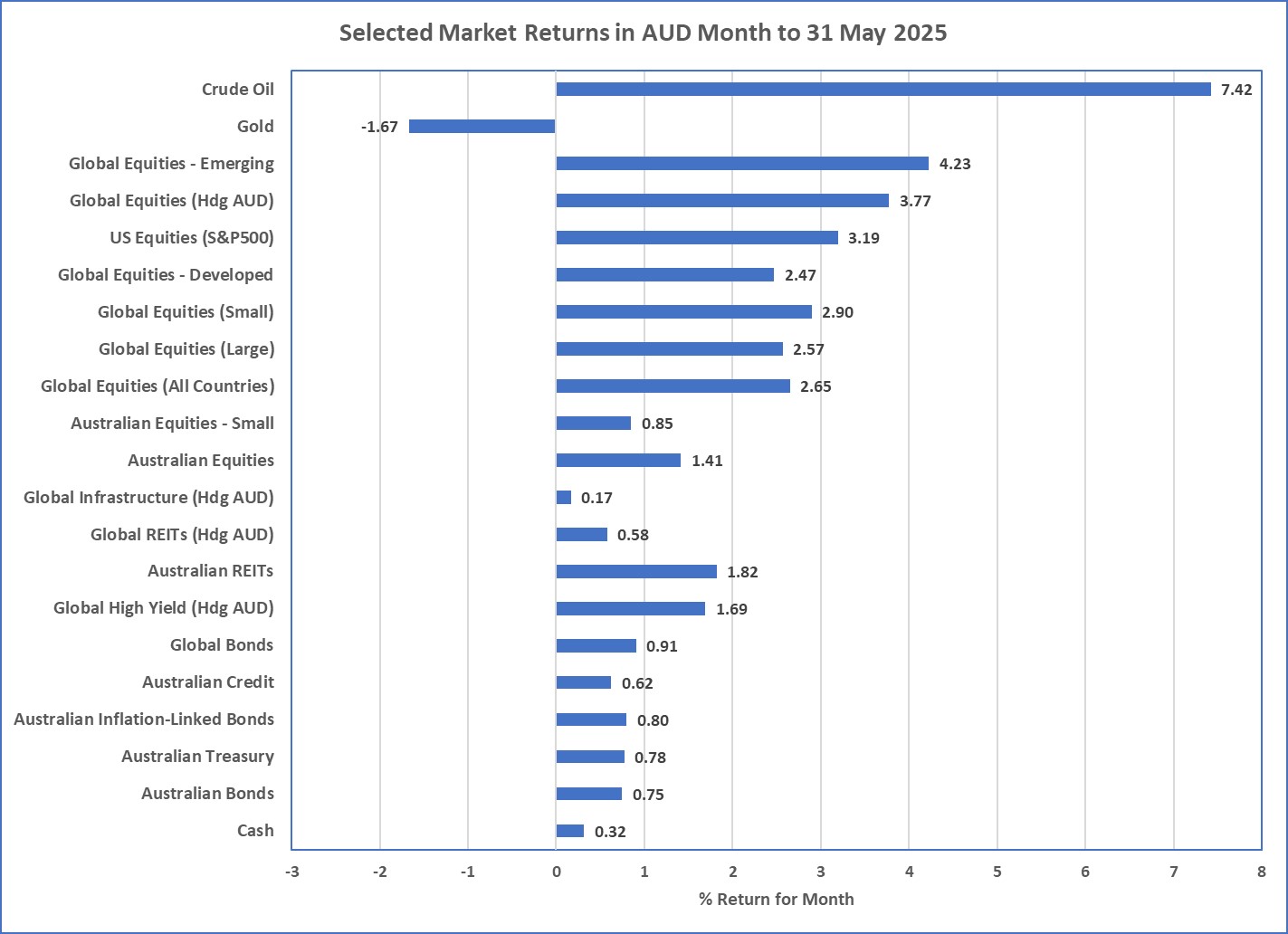

Chart 1 … A good month for all but gold bugs

Source: Morningstar

What happened last month?

Markets & Economy

- Geopolitical issues continued to be the dominant market issue, but tariffs took a backseat to the Middle East, where Israel and Iran endured a 12-day war which was effectively finished by the USA bombing some nuclear facilities in Iran over concern about them progressing towards building nuclear weapons. Given Iran is one of the world’s biggest oil producers, it should be unsurprising that the Oil price increased by around 7.5% to outperform all asset classes and increase the costs of petrol for us all.

- Despite this conflict, it was very much a risk-on month as global sharemarkets performed very well. Developed markets (MSCI World) was up around 2.5% and emerging markets were up around 4.2%. The Australian sharemarket didn’t fare quite as well but still produced a positive 1.4%. Real assets, Bonds and Cash produced small but still positive returns.

- Economic growth is currently slightly weaker than usual around the world and short term growth expectations are also generally lower than recently experienced. This has helped keep inflation down and the inflation problems of 2022-23 appear largely in the background, although USA-imposed tariffs may change that … for the USA more than any other. Despite lower inflation amongst developed countries only the European Central Bank reduced its cash rates (by 25bps), down to 2.6%.

Outlook …still no change … increase in market volatility and lower cash rates most likely

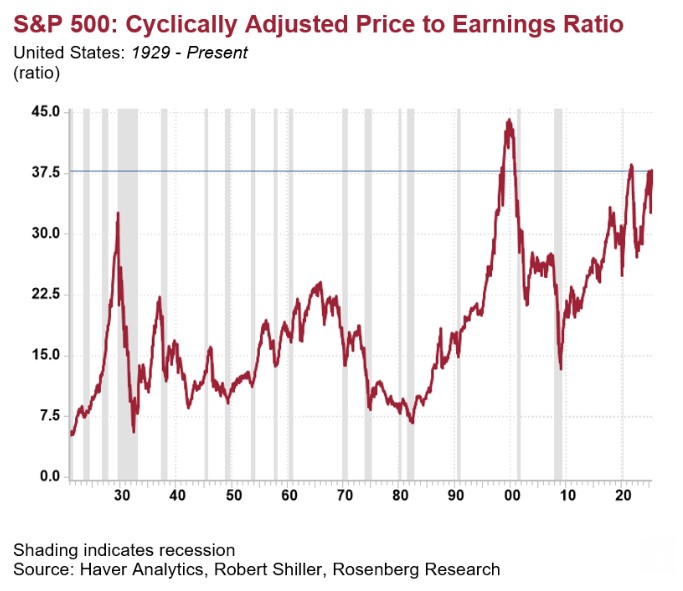

- Page 5 of this report shows USA to be near the most expensive sharemarket in the world and Page 4 shows that in the past, when the CAPE ratio has been over 35 (which it currently is), the forward returns (from 1 year to 10 years) have been negative.

- The tariff agenda is still in play and their likely return this quarter, after a short hiatus, will not be a good result for the global economy nor short-term USA inflation which may be higher than desired. Despite US Government rhetoric, their Big Beautiful Budget Bill is unlikely to significantly reduce the impact of the potential biggest tariff hike in 20 years, so the Deferal Reserve are expected to be cautious and remain on the sidelines with no changes.

- Inflation in Australia is low (2.4%) and current pricing suggests the Reserve Bank of Australia will reduce rates to around 3% by the end of 2025. The US tariff regime may actually result in some deflationary pressure in Australia as China looks to dump cheap goods.

- Overall, the general portfolio preferences are unchanged and centres on diversification. Volatile markets are likely to continue, and diversification continues to be essential in this environment, whether shares, bonds, real assets, as well as across regions and broader asset class levels. Over the long-term, we believe valuation matters and this continues to be another central theme for investment today.

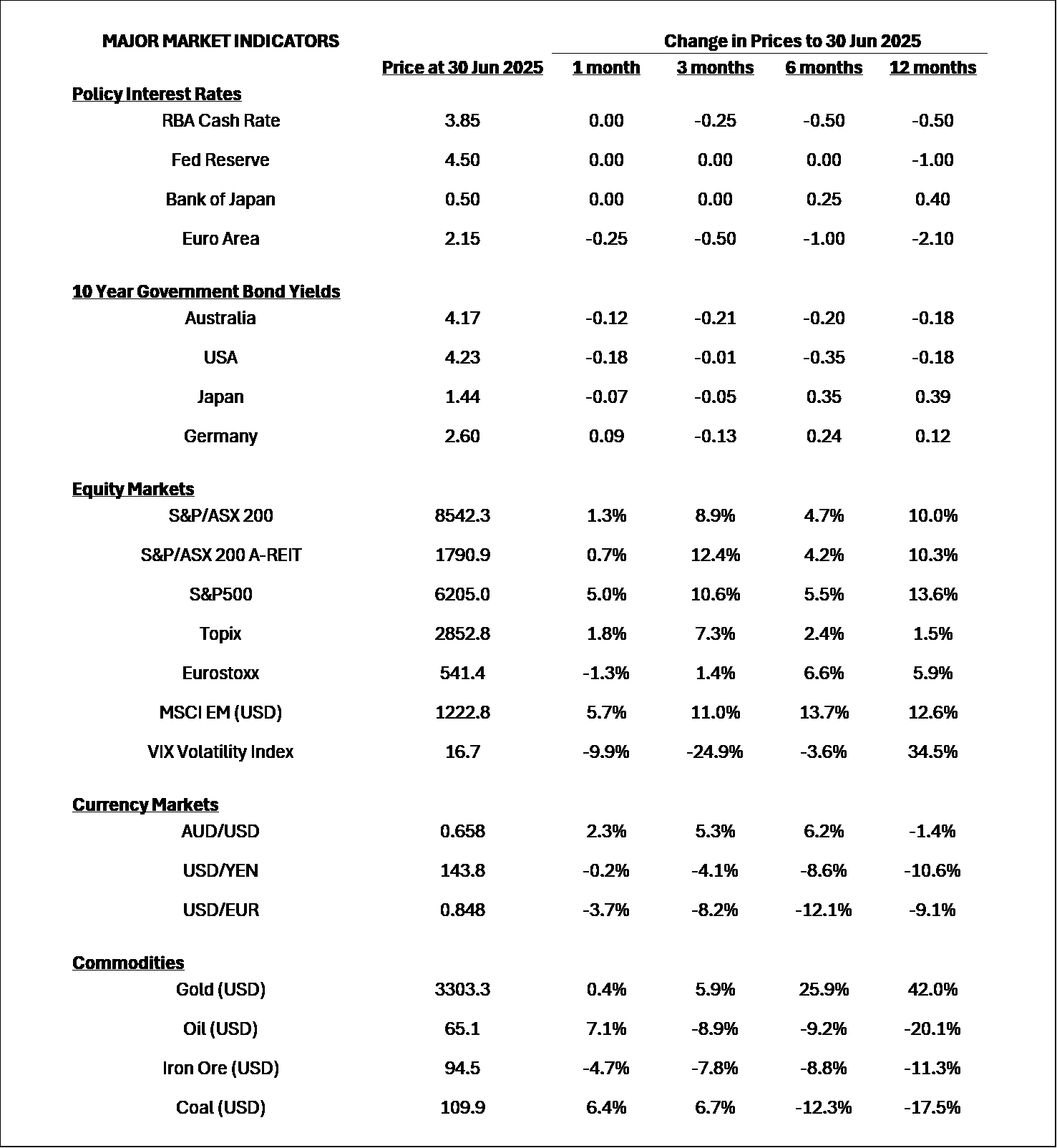

Major Market Indicators

Sources: Morningstar, Trading Economics, Reserve Bank of Australia

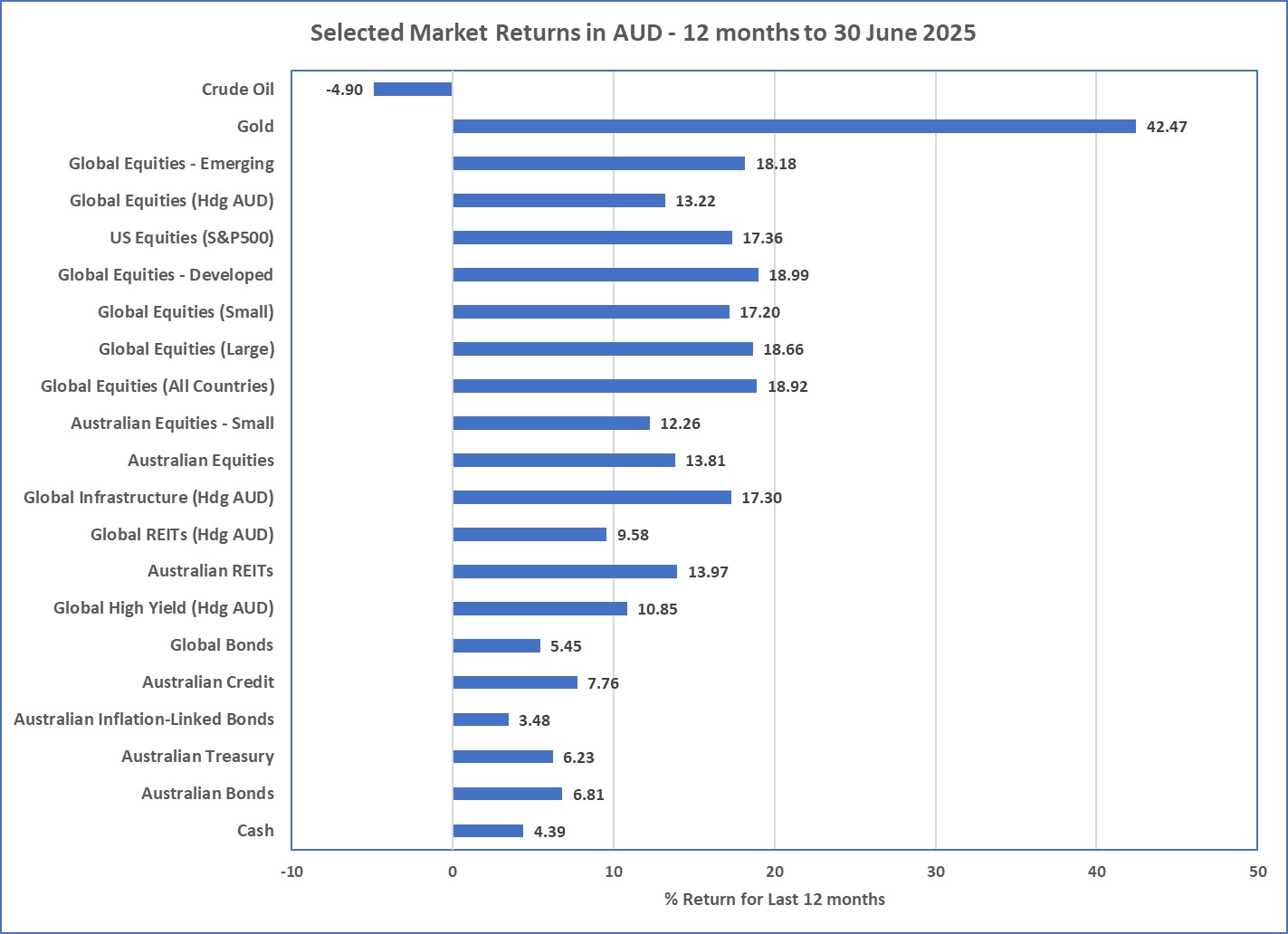

Source: Morningstar

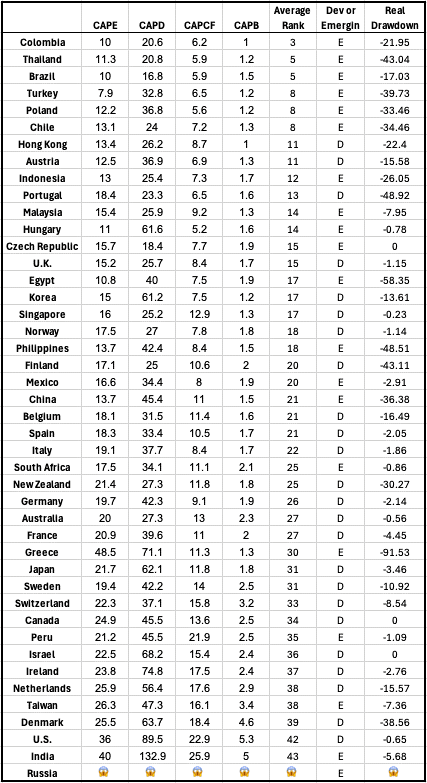

Sharemarket Valuation Ratios – 30 June 2025

Source: Idea Farm

McConachie Stedman Financial Planning Pty Ltd is a Corporate Authorised Representative of MCS Financial Planning Pty Ltd | ABN 11 677 710

600 | AFSL 560040

General Advice Warning

The information provided in this article is for general information purposes only and is not intended to and does not constitute formal

taxation, financial or accounting advice. McConachie Stedman does not give any guarantee, warranty or make any representation that the

information is fit for a particular purpose. As such, you should not make any investment or other financial decision in reliance upon the

information set out in this correspondence and should seek professional advice on the financial, legal and taxation implications before

making any such decisions