Market Snapshot: March 2021

In summary

- The vaccine continues to be rolled out around the world with greatest success in the USA where over 20% of the population is fully vaccinated. That said, there does appear to be a third wave of new cases coming out of Europe with France recently moving back into lockdown.

- New COVID-19 variants (including vaccine-resistant ones) and vaccine complacency is the current major risk to pandemic recovery.

- Bond markets mostly settled during March, although USA bond yields continued to increase, and this provided a platform for strong returns from Australian REITs, Listed Infrastructure, and equity markets in most developed countries.

- The higher interest rates are a reflection of a stronger global economic with the world economy expected to grow near 5.6% and the USA in excess of 6%.

- The high relative bond yields in USA resulted in a stronger US Dollar and most currencies, including the Australian dollar, weakened.

- Looking ahead, as repetitive as this message has been, recovery from COVID-19 and now its vaccine rollout is key to markets and economic recovery. New variants are a major risk to future vaccine effectiveness and ensuring high levels of vaccination is crucial to shifting towards herd immunity.

- Our portfolios have maintained their neutral position on risky assets and shifting away from cash assets towards higher yielding bonds is currently preferred.

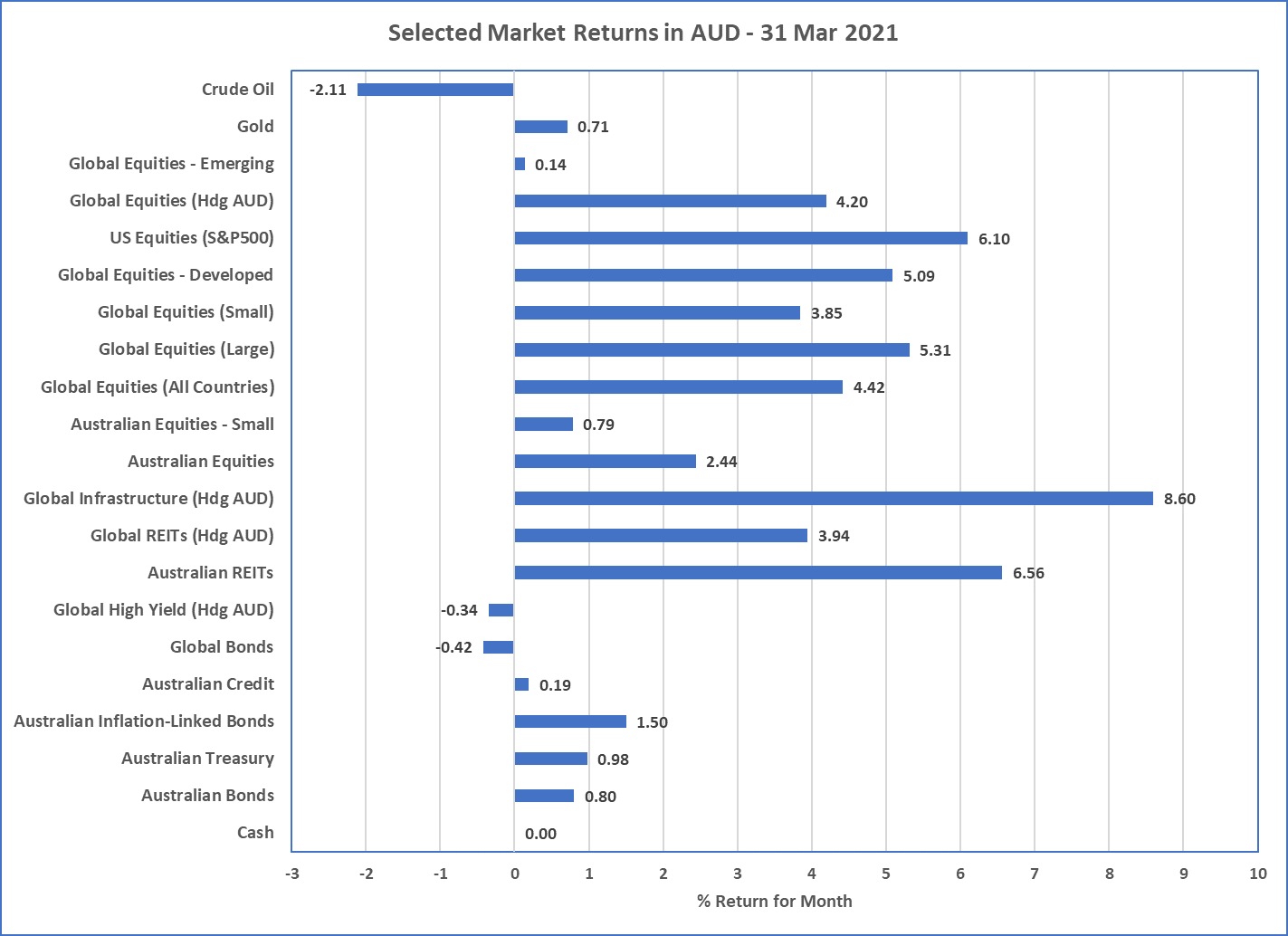

Chart 1: February markets were mostly positive for risky assets and not so defensive assets

Sources: Morningstar Direct

What happened in March?

Pandemic

Vaccines continue to roll out, but complacency remains a risk

- France has shifted into its third lockdown as the number of cases starts to significantly increase around Europe with between 20,000 and 60,000 cases per day coming from France, Italy, Poland, and Turkey.

- USA case numbers are also starting to increase but their strong vaccine rollout with more than 20% of the population fully vaccinated loos promising.

- The biggest risks currently appear to be focused on complacency around the rollout of the vaccine and insufficient number of people getting the vaccine. This could result in new variants being less susceptible to the vaccine, resulting in further increases and deaths, lockdowns, etc. At this stage, the vaccines all appear to be highly effective so it is up to the ability of a coordinated rollout by governments and pharmaceutical companies.

Markets

Settling down a little

- With bond markets (i.e. interest rate markets) mostly settling down, it provided the opportunity for the riskier assets to also settle and revert to their previously strong momentum.

- US Bond Yields did continue to increase (US 10 Year Bond increased by more than 0.30%) as Joe Biden’s massive Fiscal Stimulus package passed through both level of congress. This resulted in a slight loss for the usual defensive asset class, Global Bonds.

- Best performers over February were the interest rate sensitive Real Assets, i.e. Listed Infrastructure and Australian REITs (both of these asset classes were the amongst worst performers in February).

- The higher US interest rates, relative to the rest of the world, resulted in a stronger US Dollar against major currencies. The Australian Dollar therefore weakened slightly to finish March down to $0.76USD.

- With the exception of Emerging Markets (which were relatively flat in AUD terms), major global equity markets had a strong March with Australian equities up almost 2.5% and Developed Market equities up a solid 5%.

Geopolitics

Fighting over vaccines

- The European Union stopped a significant COVID-19 vaccine shipment to Australia meaning Australia’s supply is low and no chance of meeting government targets, whilst Europe will use this excess to increase their current slow rollout. There did not appear to be a great deal of disagreement as Australia took the high road given it is clearly better placed than Europe when it comes to current ability of dealing with the pandemic.

- Joe Biden has started to assert his views on some of the US adversaries, including acknowledging Vladimir Putin is a “murderer”. Clearly this will do little to help relations, but the clear objective is to counter Russia’s bad behaviour in recent years including their meddling in US elections.

Outlook

-

The economic outlook for the world and its biggest economy, USA, is very strong. Many economists predict Real GDP Growth in the USA to be

around 6%, with major investment banks Goldman Sachs and Morgan Stanley, predicting growth in excess of 7%. Most major global economic

organisations, including the IMF, World Bank, and OECD, are predicting global economic growth to be around 5.6% for 2021.

- It is worth noting that this economic growth is expected to be mixed as different countries struggle at different levels with the resolution of the pandemic.

- With strong economic growth outlook, albeit from a low base that was the 2020 recession, financial markets are increasingly looking like justifying their high valuation levels. That said, the US sharemarket is still significantly more expensive than the rest of the world and does present a high valuation risk, and therefore we maintain low long term expected return potential.

- The low cash interest rates provided by central banks around the world are likely to provide some support for high valuations for some time yet and will likely keep funds flowing into the riskier property and equity asset classes as investors chase better than inflation returns. This will create bursts of volatility from time to time as markets are likely to occasionally heat up too quickly thereby needing to occasionally cool down. Predicting when this will happen is near impossible but maintaining a long term view and avoiding short term expectations means that returns over the next 5 to 10 years are likely to be low and no more than 5% to 8%pa on average for global equity markets.

- From a portfolio perspective, the slightly higher bond yields has resulted in a preferred shift away from low interest rate cash and towards bonds. Given high equity market valuations, there has been little incentive to increase allocations towards these risky assets and maintaining a neutral position between risky and not-risky assets is preferred for now (although higher equity market volatility would be unsurprising).

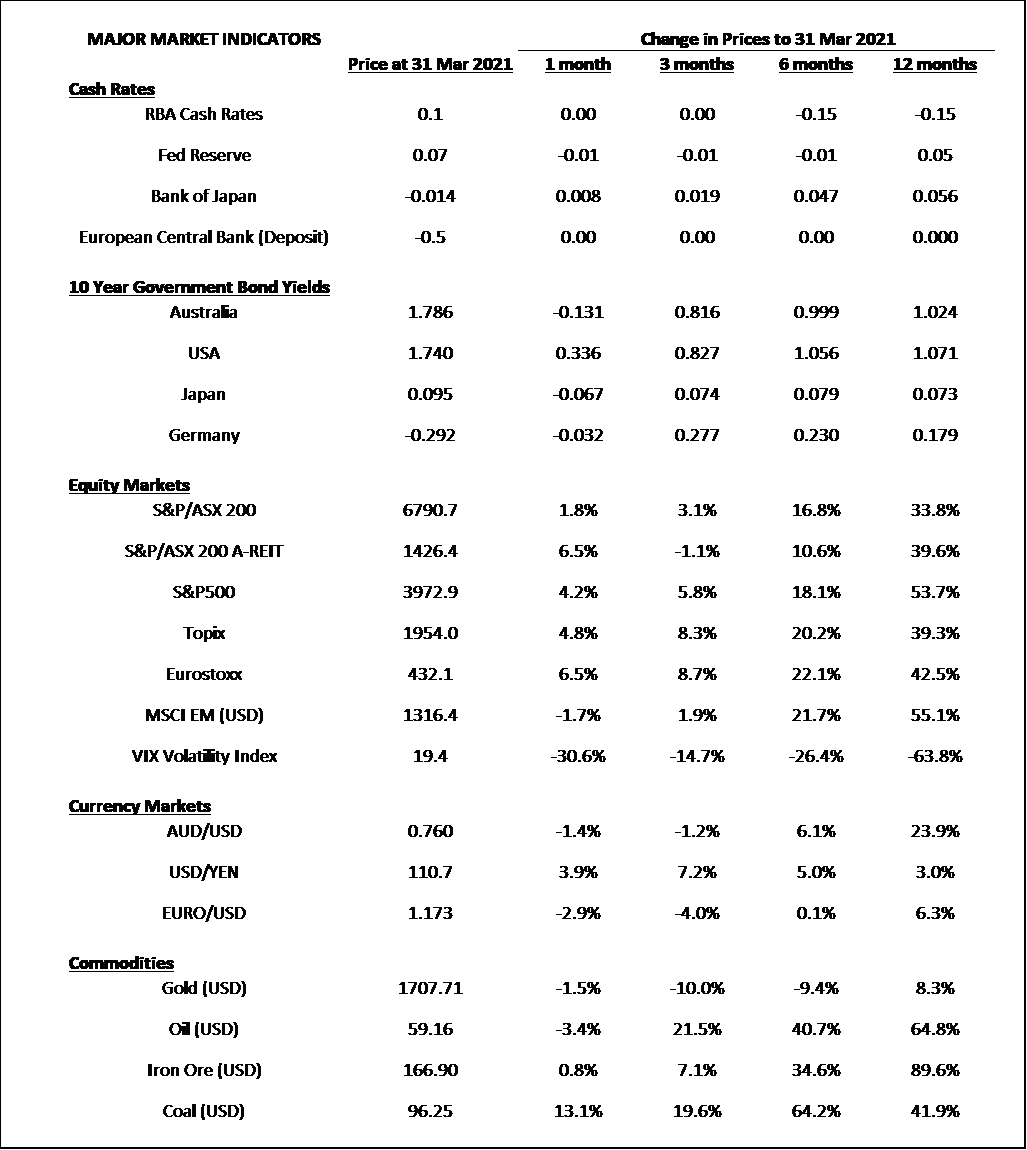

Major Market Indicators

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL 491619