Market Snapshot: March 2022

In summary

-

High inflation continues to be the main story influencing higher cash rates from central banks as well as presenting the potential for an

economic recession in USA.

- Whilst shorter term bond yields increase with higher cash rates, the main question is, will longer term bond yields increase further creating more pain for conservative investors? We think there is definitely a chance for further increases but recessionary concerns should keep them relatively stable for now.

- The Pandemic numbers continue to improve and its lesser role in financial markets is somewhat confirmed over March with the lowest mortality rates since March 2020.

- The Russian/Ukraine is keeping food and energy prices high which will flow into higher inflation on top of the other inflationary issues (e.g. supply constraints, unmet demand for goods). This may maintain Australian dollar strength.

- All in all, equity volatility is expected to continue over the short term as markets adjust to this new post-pandemic, higher inflationary world.

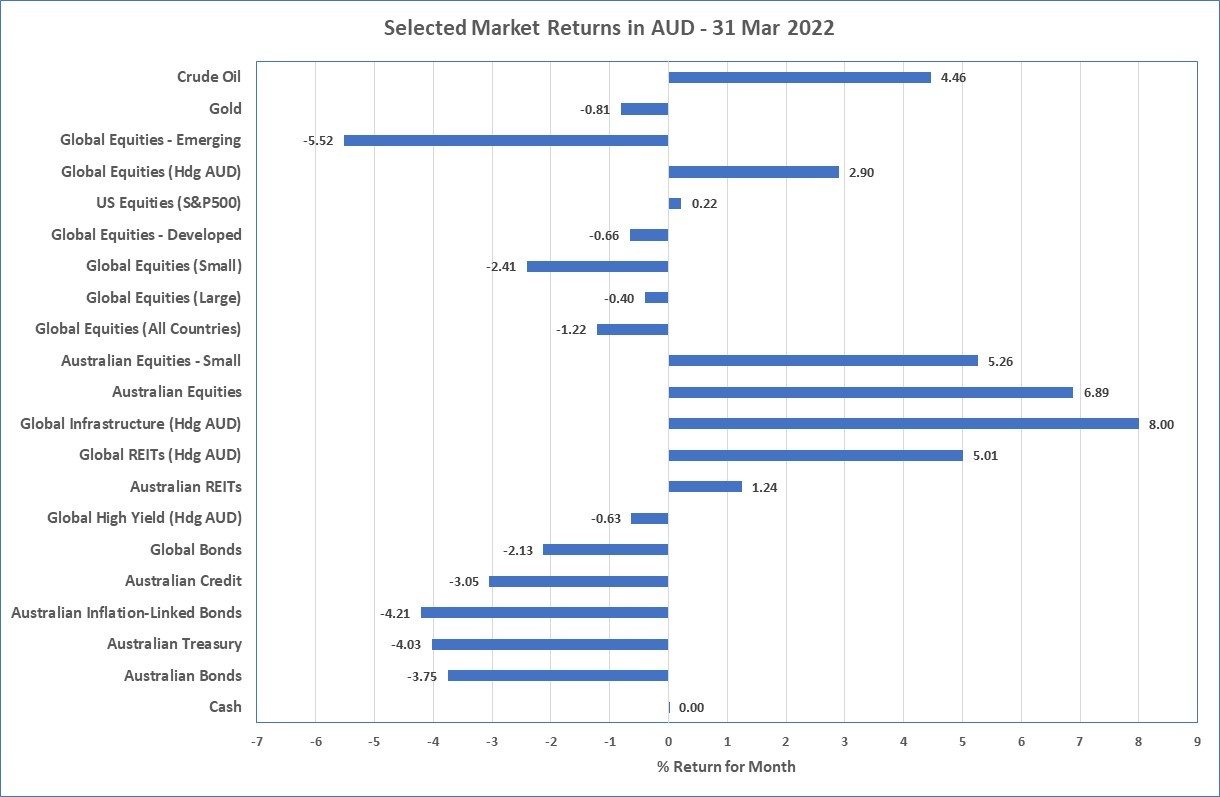

Chart 1: Another difficult month in traditional asset classes

Sources: Morningstar

What happened in March?

Pandemic

Lowest Death Rates since the beginning

- Whilst COVID case frequency continues at higher levels since any time prior to 2022, global mortality rates are at their lowest since 31 March 2020, which was only 3 weeks after the WHO declared COVID-19 a global pandemic.

- Whilst there is a recent announcement of a new Omicron variant by China, financial markets and most governments around the world continue their return to normal, are focused on non-COVID risks as vaccines have demonstrated their effectiveness. That said, complacency continues to be a risk and more boosters appear to a requirement of a new normal.

Markets

Small risk-on bounce

- US equity markets have recovered around half of 2022 losses after hitting their low during mid-March. This was the case for both the S&P 500 and the tech-heavy NASDAQ index.

- The Australian equity market (S&P/ASX 200) was one of the better performing markets with a strong ~7% increase during March, along with

the listed Property and Infrastructure markets which increased between 5% and 8%.

- These markets generally pay a higher dividend compared to other international markets, and in the case of Australia, there is a strong materials sector which is benefitting from higher commodity prices.

-

The Russian invasion of Ukraine resulted in sanctions on Russia. As a large exporter of energy, metals, and agricultural products; food and

energy prices have increased sharply.

- As another commodity exporter, this saw the Australian dollar increase against the US Dollar by over 4% during March, which also resulted in muted unhedged global returns for Australian investors.

- Another impact of the Russian invasion was continued decline in Emerging Market equities which decline by more than 5% in Australian dollar terms.

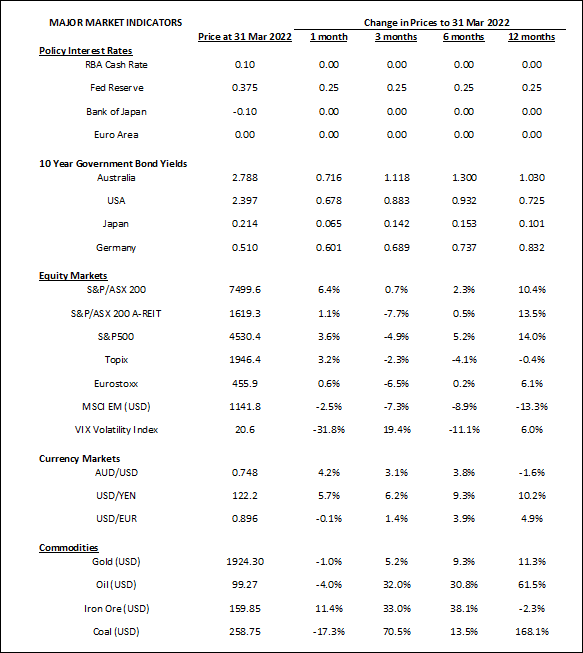

- In bond markets, the biggest news was Fed’s first increase in cash rates since the pandemic began. This contributed to higher longer term bond yields, therefore lower prices, around the world including Australia. They indicated 5 more increases in 2022 are likely.

Economy

US Economic Recession probability rises

-

Headline inflation continues to roar along in US (7.9%) and Europe (Euro Area – 7.9%, UK – 6.2%) and there doesn’t appear any sign of

letting up soon so higher cash rates, as the US Federal Reserve indicated, should be expected.

- Australia’s headline inflation is currently a little high (3.5%) but expectations are it will be getting higher again and quickly. RBA has been steady as wage inflation is low.

- Inflation concerns are made worse with low levels of unemployment expected to increase wage inflation.

- Whilst the latest economic growth results are strong around the world (albeit relatively weak in China at 4%), the high inflation combined with higher interest rates are expected to slow growth into the future. This will possibly result in more stable longer term bonds.

Outlook

-

The main trends from last month remain the same. The Russian invasion of Ukraine will likely keep energy prices high, leading to higher

inflation given energy is a major input to everything.

- This means higher short-term cash and bond yields are still more likely than not.

- With longer term bond yields in the US sneaking lower than 2- and 3-year bond yields, this leading indicator often precedes recession. So, whilst shorter term rates are a high probability, the same can’t be said for longer term bond yields which may reduce in a recession meaning bonds continue to play an important defensive role in portfolios … and equity market volatility is likely to be high.

- The post-pandemic world is currently shaping up to be one of higher inflation, higher bond yields, and greater equity market volatility.

Major Market Indicators

Sources: Tradingview, Morningstar, Trading Economics, Reserve Bank of Australia

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL 491619