Market Snapshot: March 2026

Summary

Iran Attack by USA and Israel will likely dominate financial markets for a few months yet

- USA and Israel attack Iran, resulting in massive energy price spikes and shortages as Iran has shown it doesn’t really need nuclear weapons as it controls a high proportion of the world’s energy supply via geography.

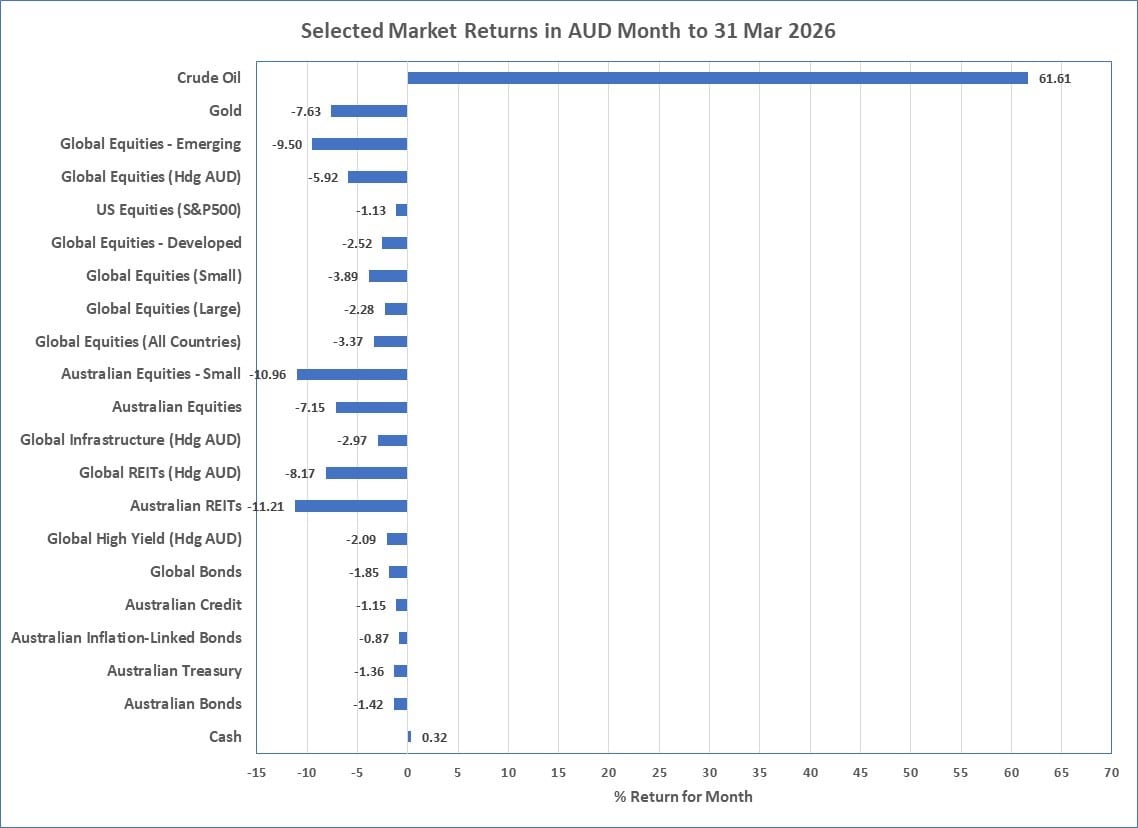

- As Chart 1 below shows, all markets, except Oil and Cash, declined over March, including the previous market-darling, Gold … which may not always be the market hedge many believe.

- Economically, the high energy prices will lead to higher goods prices, therefore higher inflation, and this may keep interest rates higher than previously expected both in Australia and around the world. That said, economic forecasts for the world are continued positive economic growth (including Australia), although it likely comes with an expectation the war will resolve sooner than later (meaning energy prices don’t persist too high for too long).

- Our core investment message remains despite persistent downside risks from high sharemarket valuation in USA and the current war(s). This means disciplined risk management rather than aggressive positioning changes. Shares continue to offer an attractive risk premium in specific markets, as do conservative bonds, but returns may be challenged from short term volatility. Avoiding panic (selling) decisions continues to be a crucial investment issue today for long-term investors.

Chart 1 … Negative returns everywhere … except an obvious one

Source: Morningstar

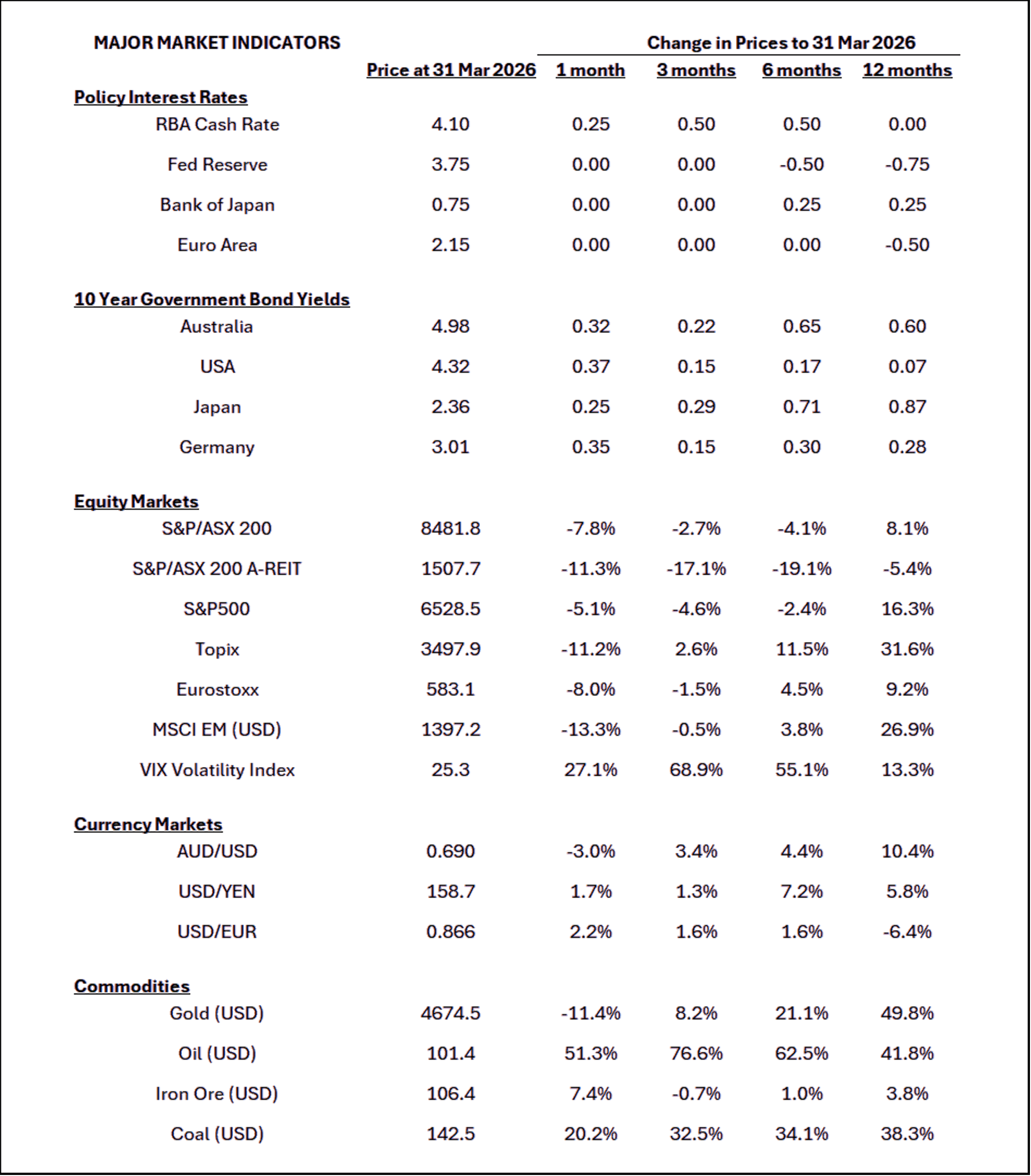

What happened last month?

Markets & Economy … USA and Israel attack Iran

-

Middle East tensions near maximised during March as USA and Israel attacked Iran, Iran retaliated by bombing Middle Eastern USA allies, and

closing the Hormuz Strait resulting in a reduction in global oil supply and massive increases in energy prices. The global oil price

benchmark, Brent, finished the month over $100USD per barrel which is an increase of more than 30% from the end of February.

- At the time of writing, there is a ceasefire which has resulted in some calming of energy, share, and bond markets. Although the calming of market volatility is likely to be temporary as the Hormuz Strait continues to have few, if any, ships passing through … so economic pressures remain.

-

High energy prices mean higher inflation as it behaves similar to a tax as it increases the price of anything that is transported. This is

usually bad for share, property, and bond markets and unsurprisingly, all declined substantially during March. MSCI World was down almost

6%, Global Property down around 8%, and Global Bonds down almost 2%. Largest price declines were in energy dependent Asian and European

markets.

- It appears only Oil and Cash increased in price during March.

- Australian markets have felt the energy price increases substantially. Inflation was already high, at 3.7%, and the higher energy prices means it will stay higher for a little longer yet. Unsurprisingly, the Reserve Bank increased its cash rate for the second time in 2026, leaving it at 4.1%.

Outlook …

- Despite the energy shock that will undoubtedly flow into higher inflation, global economic growth is forecast to be moderate in 2026, at ~2.5% to 2.7%, which is moderate growth only a little lower than the 2025 calendar year.

- Some of the shorter market expectations will depend on the current Middle East tensions and these appear to be well from finished. We believe it is impossible to time these markets and despite current volatility we believe it is prudent to stay invested. It is not uncommon that markets can bounce back quickly following geopolitical events, making market timing a risky proposition if investing for the longer term.

- At the time of writing, there appears the increased possibility of a collapse in US-Iran talks following a recently announced cease-fire, resulting in surging oil prices again.

-

For now, there is likely to be a pause in reducing global cash rates and ongoing market volatility across all markets is likely to

continue.

-

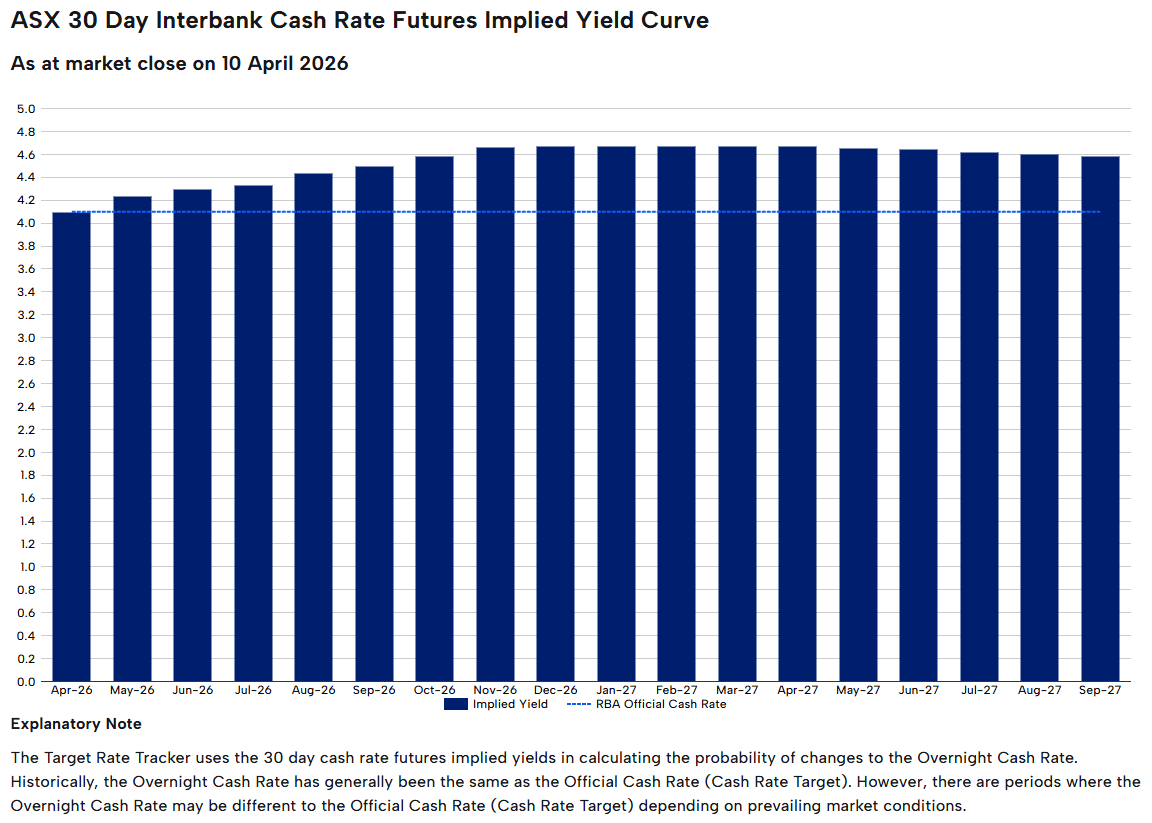

In Australia, markets currently suggest the rate rises are not finished yet, and price in another 3 rises by the end of the year.

-

In Australia, markets currently suggest the rate rises are not finished yet, and price in another 3 rises by the end of the year.

- Diversification continues to be essential. Maintaining a balance between domestic and global exposures remains a prudent approach as 2026 unfolds. Entering new investment positions are best approached using a dollar-cost averaging approach and rebalancing as pricing opportunities arise continues to be appropriate for established portfolios.

Major Market Indicators

Sources: Morningstar, Trading Economics, Reserve Bank of Australia

Market Expectations of future RBA Cash Rates

Following the Iran attack, Australian Cash rates are expected to go even higher than previously expected:

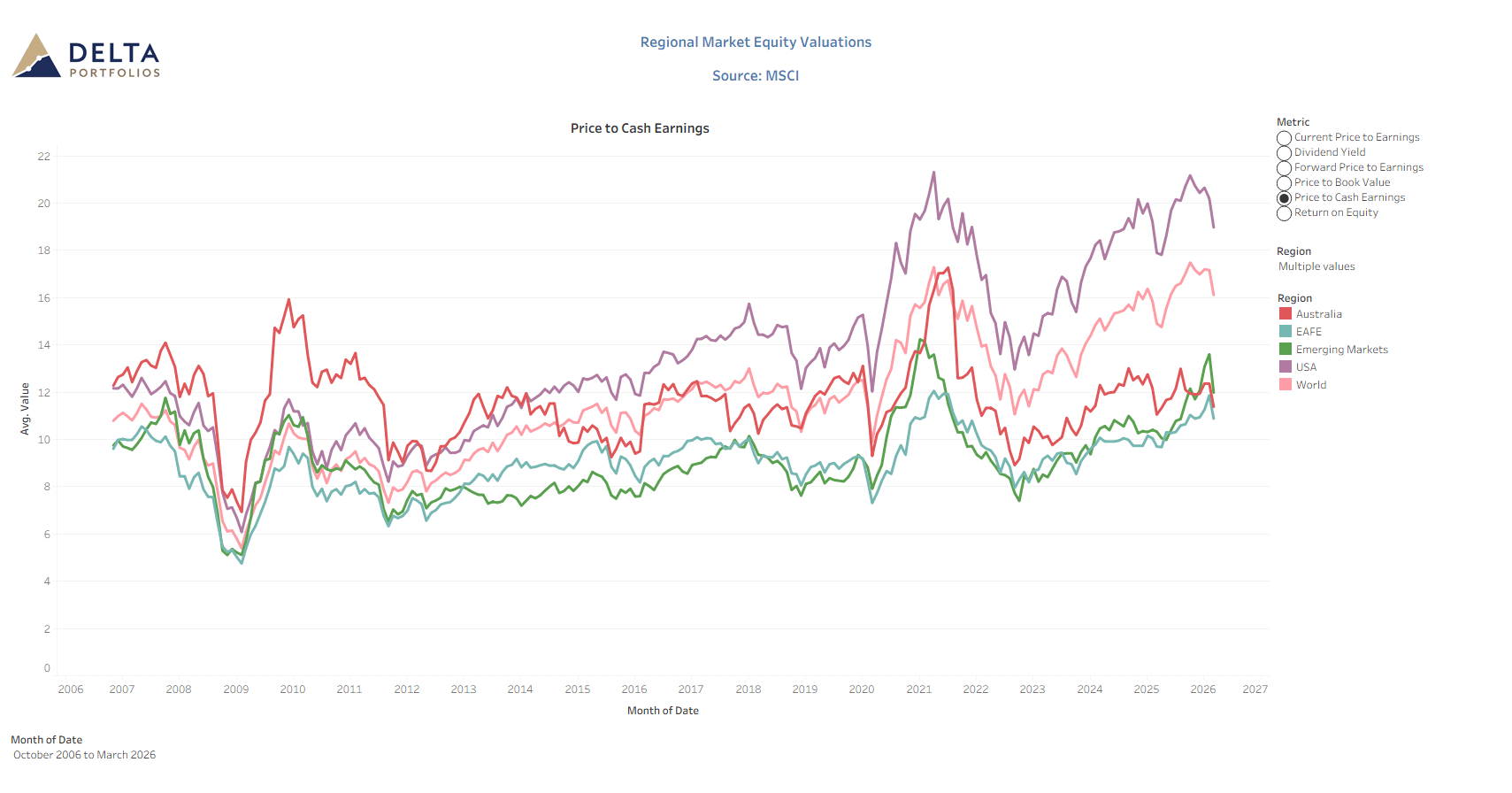

USA still on the high side of valuations … although has dropped significantly

McConachie Stedman Financial Planning Pty Ltd is a Corporate Authorised Representative of MCS Financial Planning Pty Ltd | ABN 11 677 710

600 | AFSL 560040

General Advice Warning

The information provided in this article is for general information purposes only and is not intended to and does not constitute formal

taxation, financial or accounting advice. McConachie Stedman does not give any guarantee, warranty or make any representation that the

information is fit for a particular purpose. As such, you should not make any investment or other financial decision in reliance upon the

information set out in this correspondence and should seek professional advice on the financial, legal and taxation implications before

making any such decisions.