Market Snapshot: May 2023

In summary

High returning sharemarkets leading into potential recession are unusual

- The global economy continues to experience high inflation and relatively low unemployment across major markets (including Australia) but there are numerous signs of economies slowing and they should continue to slow for a couple of quarters yet.

- Central Banks have shown they will be relentless in combat inflation and at the cost of short-term economic pain. The USA and European bond markets continue to point to recession, possibly later in 2023 in USA, and Australia’s yield curve suggests weak growth too.

- It was a challenging investment period in May unless holding US Dollars and US stocks. Returns in 2023 for Large US Tech Companies have been high and this is where the current major risks lie.

-

Looking ahead, the primary thesis remains. Our market expectations demand caution on equity markets as valuations do not reflect recession

possibilities. Higher investment market volatility across all asset classes is expected as the global economy slows during 2023.

- From a valuation perspective, we prefer to be underweighted in the most expensive markets which continue to be US Equities (particularly growth/tech) and High Yield.

- High quality securities (defined by good profitability and strong balance sheets) may provide some recession protection ... which supports some (but not all) US Tech

- In recent months we shifted to a preference for shorter duration in debt markets as bond yields reduce to well below cash interest rates but, unlike recent times, still believe Bonds will provide protection to equity market volatility in 2023.

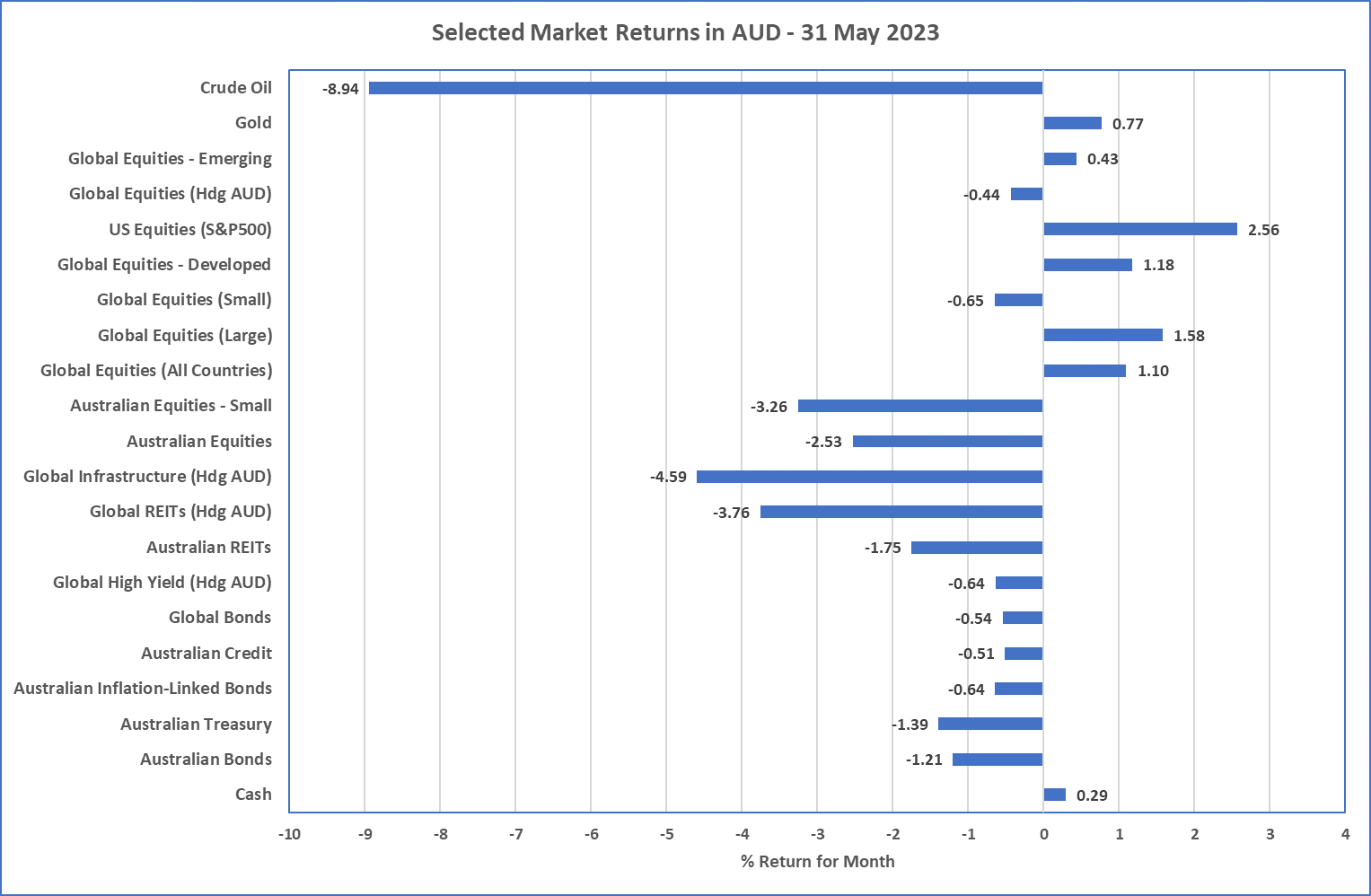

Chart 1: Tough month for most asset classes except US Dollar

Source: Morningstar

What happened last month?

Markets & Economy

Inflation expectations persist, cash rates up and only the US Dollar liked it

- Inflation continues to take the economic headlines as central banks around the world continue to increase rates to slow their respective economies and force lower inflation from lower demand.

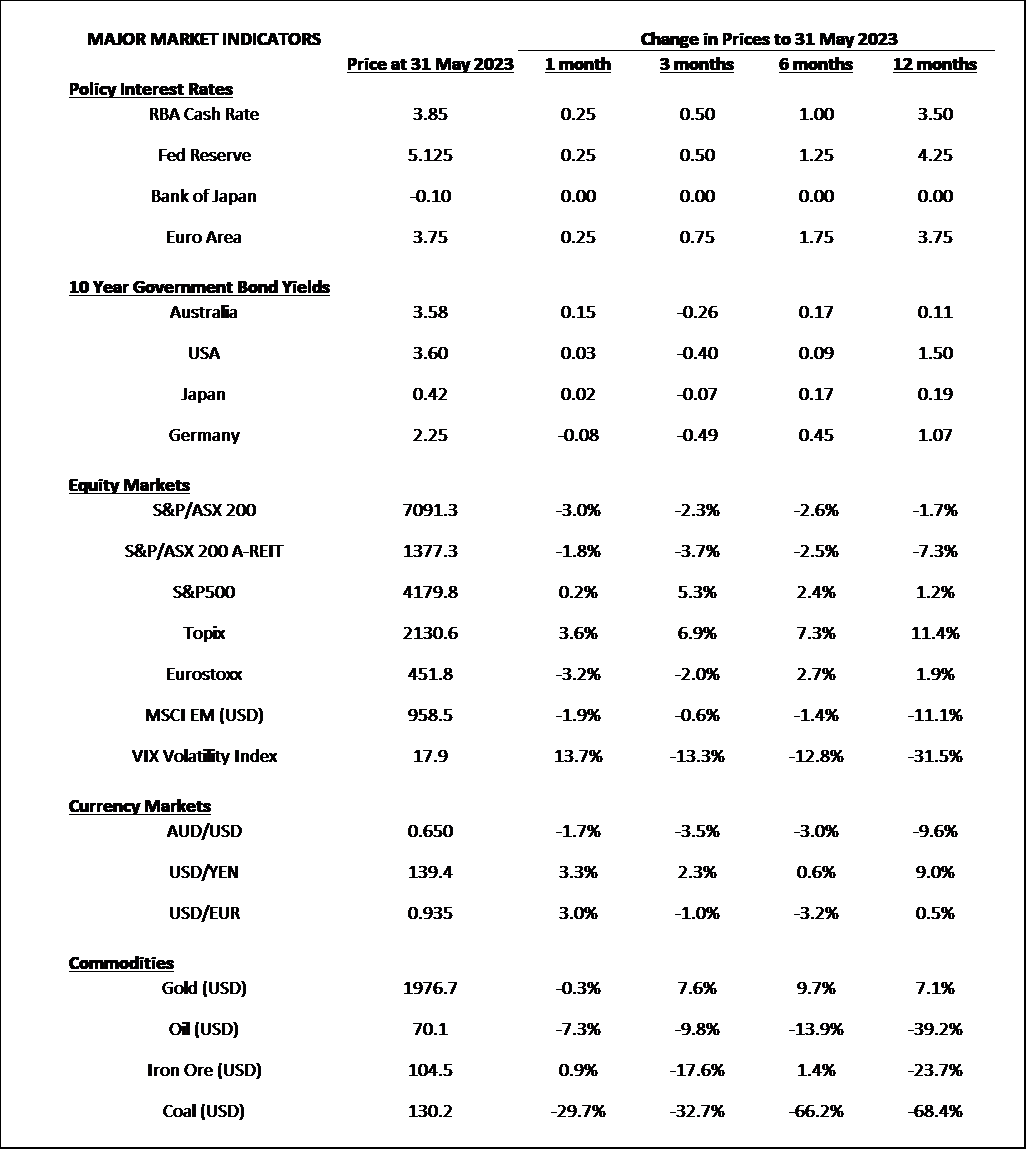

- These “still too high” inflation levels are currently at 4.9% in USA, 7% in Australia, and 6.1% in the Euro area. Japan’s inflation is still near 30-year highs at 3.5%, but the Bank of Japan has held tight keeping zero cash rates and maximum 0.5% 10-year bond yields.

- During May, cash rates rose another 0.25% in USA, 0.25% in Australia, and 0.25% in the Euro area, to now be at levels somewhat inconceivable a couple of years ago at 5% to 5.25%, 3.85%, and 3.75%, respectively. It’s worth pointing out Australia’s central bank, RBA, increased another 25bps at its 6 June meeting, to now sit at 4.1% … the highest cash rate since 2012.

- These central bank cash rate rises have come as somewhat of a surprise to many markets resulting in benign to poor returns across most asset classes. The strongest gains came from those who held US Dollars which strengthened between 1.5% to 3.5% across most major currencies…hence unhedged global equities performed positively (>1%) in May.

- Bond markets generally produced slightly negative returns as yields increased. This was possibly the markets’ view that inflation may be more sustainable then originally expected. That said, yield curves in USA and Europe are currently negatively sloping suggesting recession is still coming.

Outlook

The higher cash rates go, the weaker the short-term outlook.

- There appears to be little reason to provide any different view from previous months and the head of this subsection summarises it well … higher cash rates are neither good for the short-term economy whilst providing higher hurdle rates for asset valuations.

- All signals continue to point to weak or volatile sharemarkets. Inflation continues at high levels, bond yield curves signal recession, interest rates continue to rise. Sharemarkets in the USA are still historically expensive with strong returns driven by the tech sector. This points us to caution, diversification, and extreme focus to avoid the disease of FOMO (fear of missing out).

- As alluded to above, valuations risks are greatest in US Equities (particularly tech) and this is our preferred underweight equities market. That said, any volatility in US Tech may still result in volatility for other parts of the market so conservative equity strategies (e.g. low volatility) are preferred. Side note – Nvidia and Amazon respectively trade at PE Ratios of 176 and 154 (7 Jun).

- Long term bond markets have settled and are yielding below Australian cash rates so our current preference is for shorter than market duration as upward pressure on Cash rates continues. As recession risks increase further longer-term bonds usually tend to perform well so it is still important to hold this diversifying asset class.

- As stated in previous monthly statements, it is essential for all portfolios to diversify across asset classes and securities with a focus on the long term. It’s been a strong 2023 for global equity returns but current valuations suggest this is highly unlikely to continue.

Major Market Indicators

Sources: Tradingview, Morningstar, Trading Economics, Reserve Bank of Australia

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL

491619