Market Snapshot: May 2026

Summary

May … not too different from April

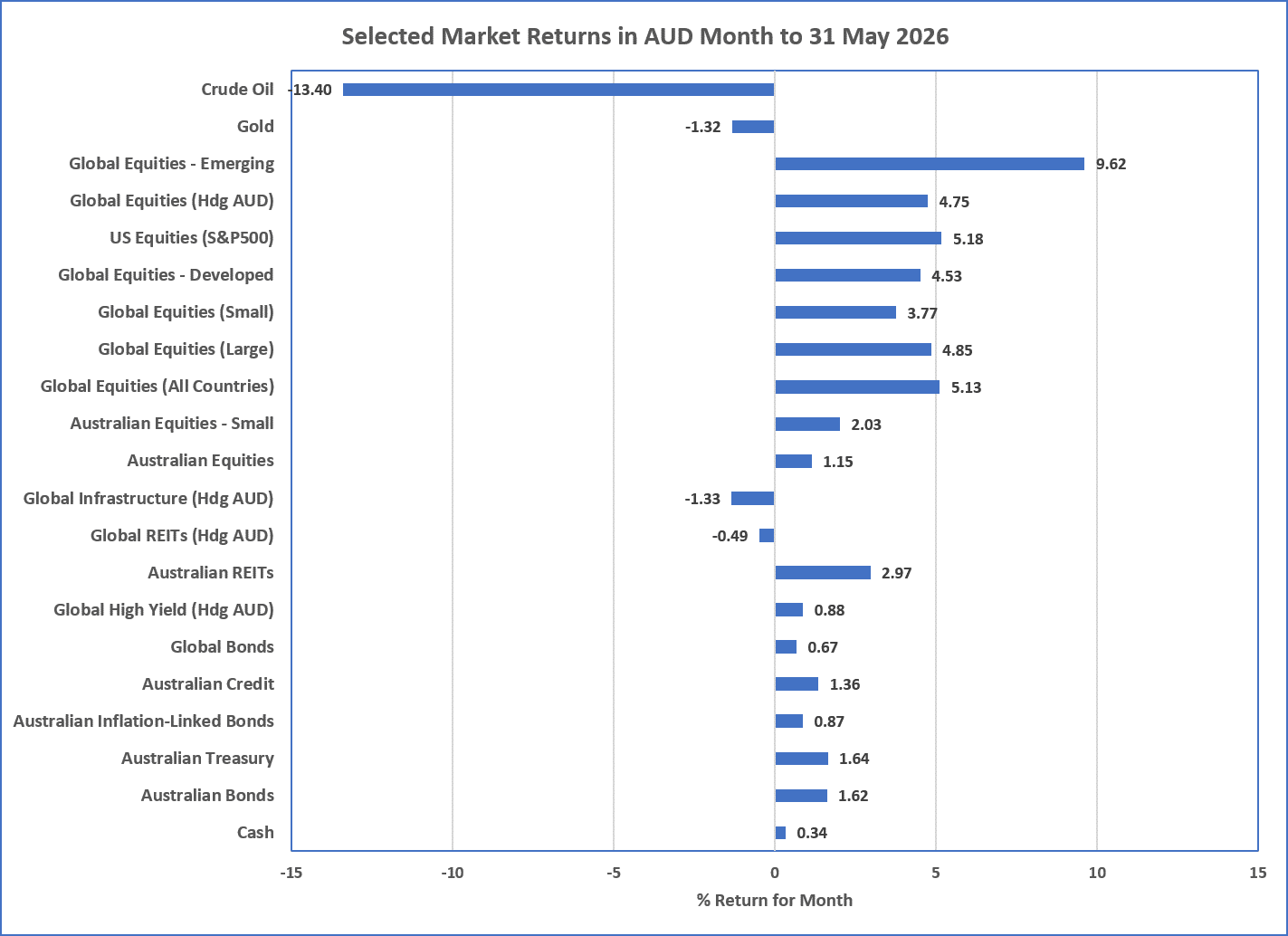

- May continued the April momentum with strong sharemarket returns but this time a near 10% return from Emerging Markets thanks to a whopping 33% return out of Korea. The US Dollar was relatively stable as were bond yields and cash rates around the world, except in Australia where the RBA increased by 25bps to 4.35%.

- As Chart 1 below shows, the “real assets” of commodities, infrastructure, and property produced mostly negative returns. This was due to weaker economics around the world, but this certainly didn’t stop the advance of various sharemarkets.

- The Iran War continues, despite numerous promises of ceasefires. Either way, it is effectively lost for the USA, as Iran continues to control the global energy supply via the Hormuz Strait. As mentioned last month, higher energy prices are expected to maintain for the remainder of 2026 feeding into higher inflation for Australia and the rest of the world. This higher inflation does not guarantee future higher cash rates or lower bond returns for all, but the RBA appears concerned about pre-existing higher inflation which is why it has increased cash rates 3 times already in 2026. Markets are pricing in 1 more rise by the RBA.

- Our core investment message remains despite persistent downside risks from high sharemarket valuation in USA and the energy crisis. This means disciplined risk management rather than aggressive positioning changes. Shares continue to offer an attractive risk premium in specific markets, as do conservative bonds, but returns may be challenged from occasional short term volatility. Avoiding panic (selling) decisions continues to be a crucial investment issue today for long-term investors.

Chart 1 … Continued Risk on … Oil comes back, the economics all looks fine?!?!?

Source: Morningstar

What happened last month?

Markets & Economy … Record highs?

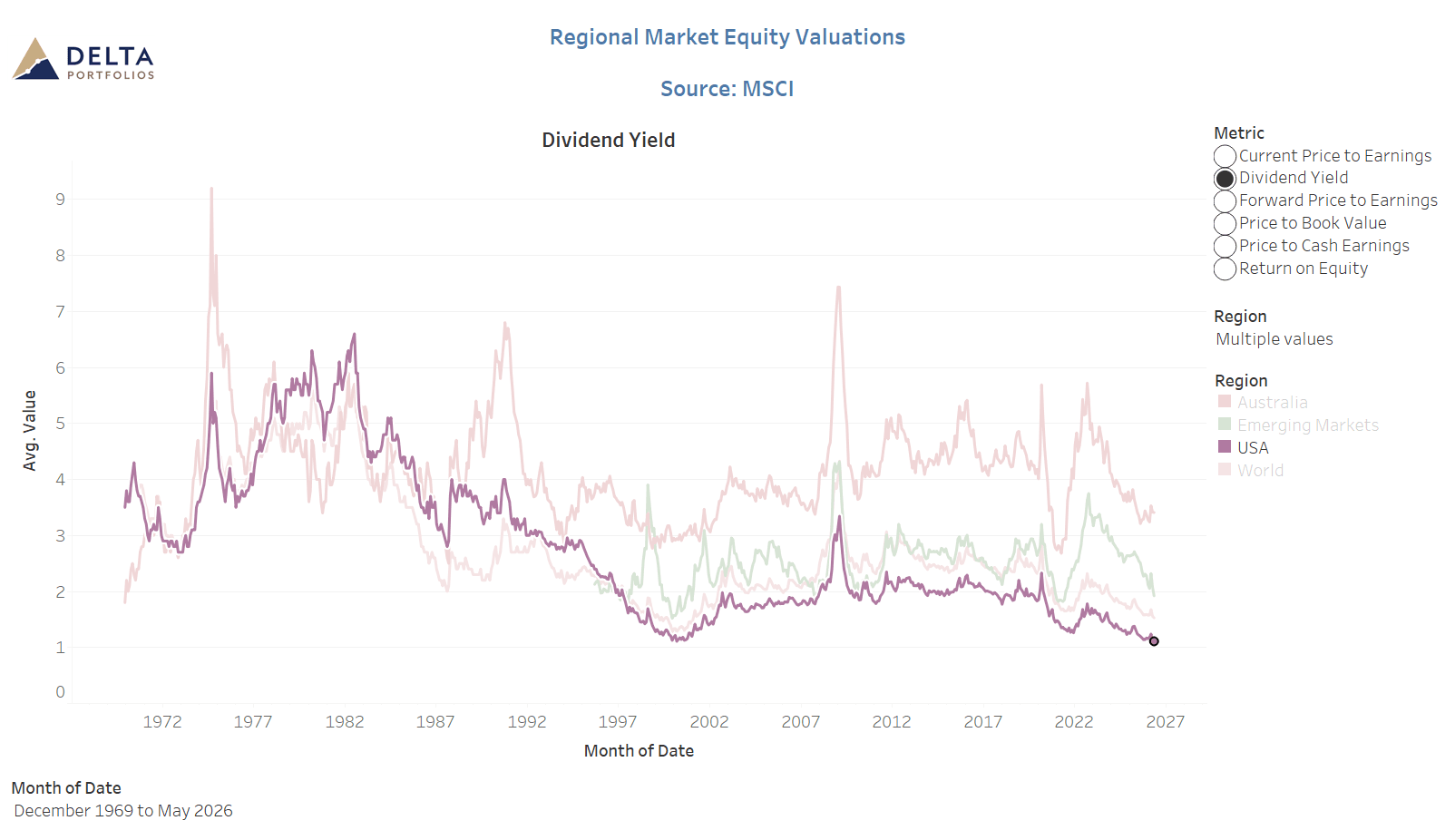

- The US sharemarket has hit record highs across several valuation metrics, which unfortunately also means a record low in terms of dividend yield. This has been driven by the continued massive spend in Artificial Intelligence-related data centres. There is increasing rhetoric around a related AI “bubble” which is also fuelled by 3 of the biggest IPOs in history, SpaceX, Anthropic, and Open AI.

- Whilst US sharemarkets establish their high prices, Emerging Markets were the best performing sub-asset class during May returning almost 10% to Australian investors. This was primarily driven by Korean and Taiwanese markets which increased a whopping 33% and 14%, respectively.

- In Australia, inflation figures continued to be higher than preferred by the RBA and they increased their cash rate for the 3rd time in 2026 to 4.35%. As expected, inflation is increasing across all major economies and should keep bond yields and cash rates higher than previously forecasted for 2026. The second issue in Australia was a budget perceived to be weak for the economy and the cash rate expectations have now reduced to only 1 more rise this year.

- At this stage, unemployment appears relatively healthy in Australia and around the world. It continues to be one of the inflation drivers in Australia adding to the RBA’s challenges. The unemployment rate will be a key indicator determining economic strength and potential interest rate movements for all economies as well as the impact of artificial intelligence.

Outlook … higher cash and sharemarket volatility

- As mentioned, markets expect only one more interest rate rise by the Reserve Bank of Australia in 2026 to a maximum of 4.6%. with bond yields around this number and early signs of a weaker economy, it appears bond yields may be potentially stable. That said, the current energy crisis or a sharemarket sell-off could change this.

- With US sharemarkets at or near record highs and record sized IPOs in the USA, there presents significant downside risks should companies not meet their high forecast growth rates. Whilst markets are generally expensive, this does not mean low returns for 2026 but longer-term expectations should be tempered and double digit returns look unlikely over the next 10 years.

- Our current beliefs are that new investors should dollar cost average into sharemarkets and long-term investors should stay invested for the long-term and expect higher volatility.

- We continue to believe portfolios should be underweight USA shares and high yield (junk) bonds due to near record high valuations. Markets continue to price in higher cash rates for Australia (~4.60% by the end of 2026), but conservative bond portfolios both global and in Australia, are providing strong expected returns over 5%pa.

- Diversification continues to be essential. Maintaining a balance between domestic and global exposures remains a prudent approach as 2026 unfolds. Rebalancing as pricing opportunities arise also continues to be appropriate for established portfolios.

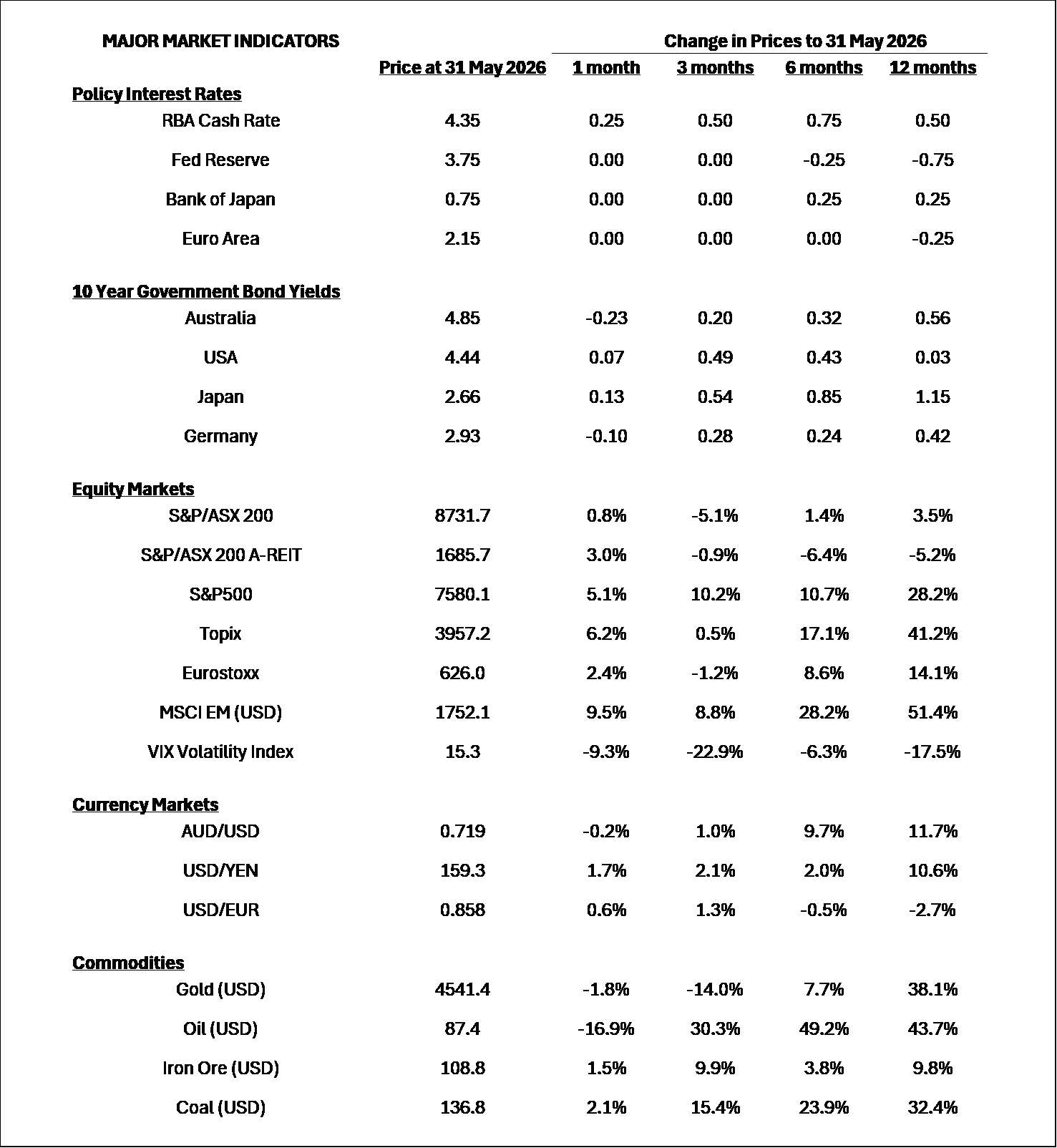

Major Market Indicators

Sources: Morningstar, Trading Economics, Reserve Bank of Australia

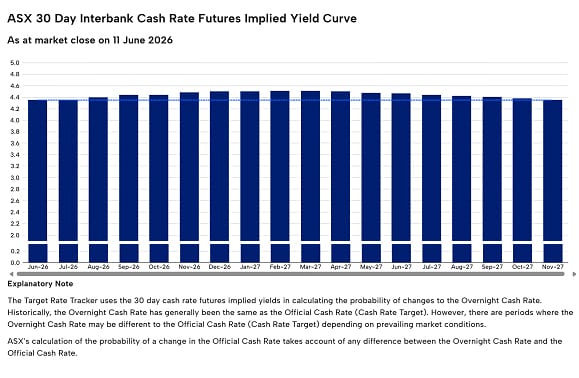

Market Expectations of future RBA Cash Rates

The RBA hiked early May has no more than 1 more increase priced in for 2026:

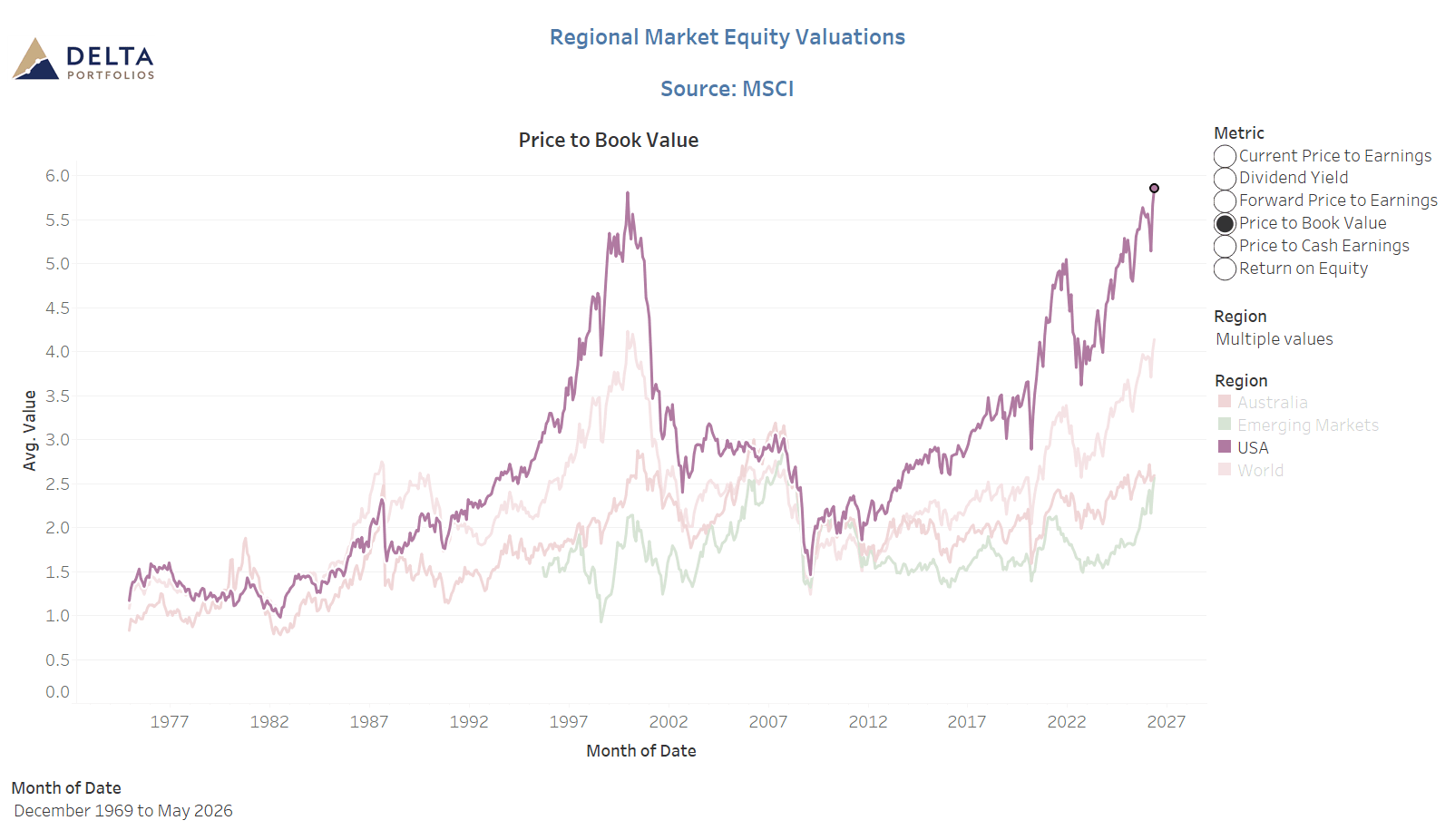

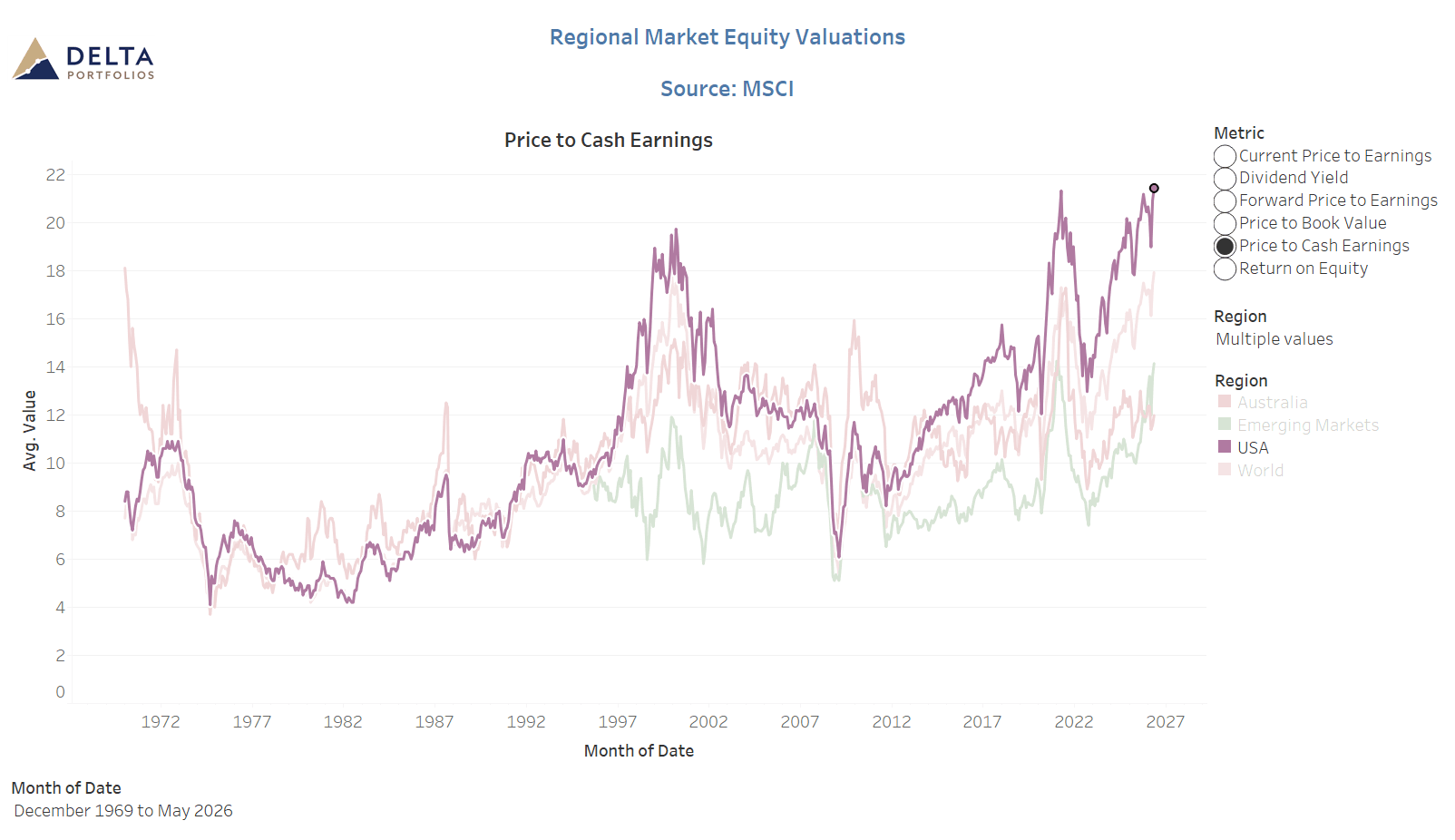

USA at record highs across price/Book, Price to Cash Earnings, and Price to Yield

The following chart shows a record low dividend yield for USA (or record high Price/Dividend Yield)

McConachie Stedman Financial Planning Pty Ltd is a Corporate Authorised Representative of MCS Financial Planning Pty Ltd | ABN 11 677 710

600 | AFSL 560040

General Advice Warning

The information provided in this article is for general information purposes only and is not intended to and does not constitute formal

taxation, financial or accounting advice. McConachie Stedman does not give any guarantee, warranty or make any representation that the

information is fit for a particular purpose. As such, you should not make any investment or other financial decision in reliance upon the

information set out in this correspondence and should seek professional advice on the financial, legal and taxation implications before

making any such decisions.