Market Snapshot: November 2021

In summary

- Last month high inflation was the concern and this time it is the new COVID-19 variant, Omicron, resulting in greater market volatility.

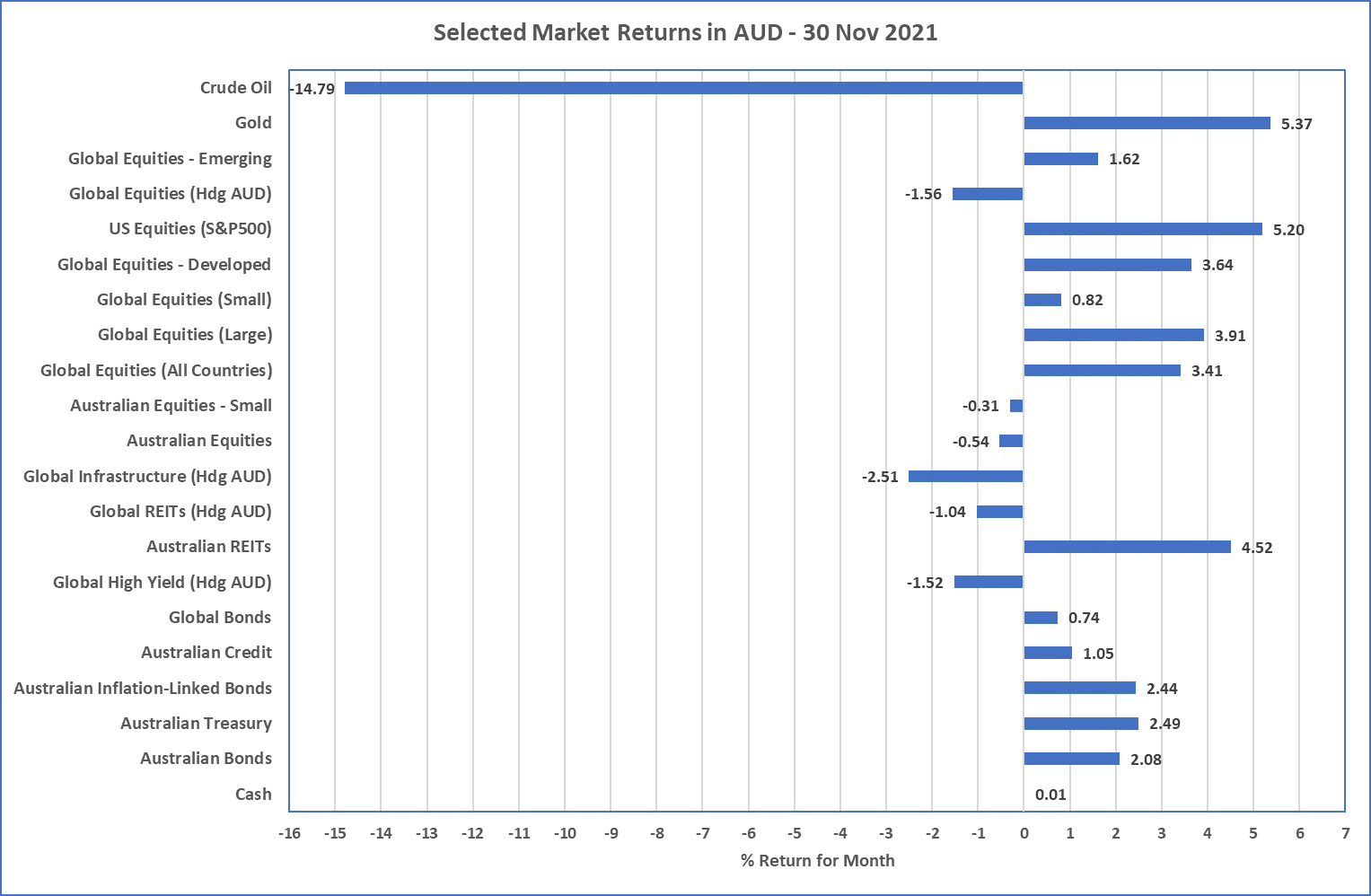

- Whilst high inflation is still coming through the economic results, lower Oil prices and Omicron have resulted in lower bond yields in Australia and USA, and a reasonably strong return month for the bond market.

- Equity markets largely paused for the month. USA equity markets remain relatively expensive, but this is not a catalyst to create portfolio changes … yet.

- The Australian Dollar was a large contributor on investor’s returns during November as it declined by over 5% against the US Dollar. This is because, along with a 50% decline in Iron Ore prices over the previous 6 months, the coinciding Bond Yield decrease of November meant there was little data supporting Australian Dollar strength. This meant unhedged equity positions (which are mostly in US Dollars) significantly outperformed hedged positions.

- Looking ahead, the current Omicron variant may be a catalyst for further equity market volatility; concerns about high inflation may also be a catalyst for equity market volatility, and considering the high valuations of US Equity markets, caution and maintaining diversification appears most prudent for now.

Chart 1: Bonds bounce back and the Australian dollar influences everything else

Sources: Morningstar Direct

What happened in November?

Pandemic

Omicron takes over from Delta as variant of concern

- Whilst its still very early days, a new COVID variant was discovered in South Africa and has been named Omicron after the 17th letter in the Greek alphabet.

- This variant is of concern as it appears to have improved the virus’s potential to resist vaccines and appears to be highly infectious. Whilst the jury is still out on how bad this variant affects people, it has created significant concern such that borders are closing, markets are increasing in volatility, and vaccine manufacturers are looking to adapt as quickly as possible.

Markets

Volatility up … but inflation outlook steadies

-

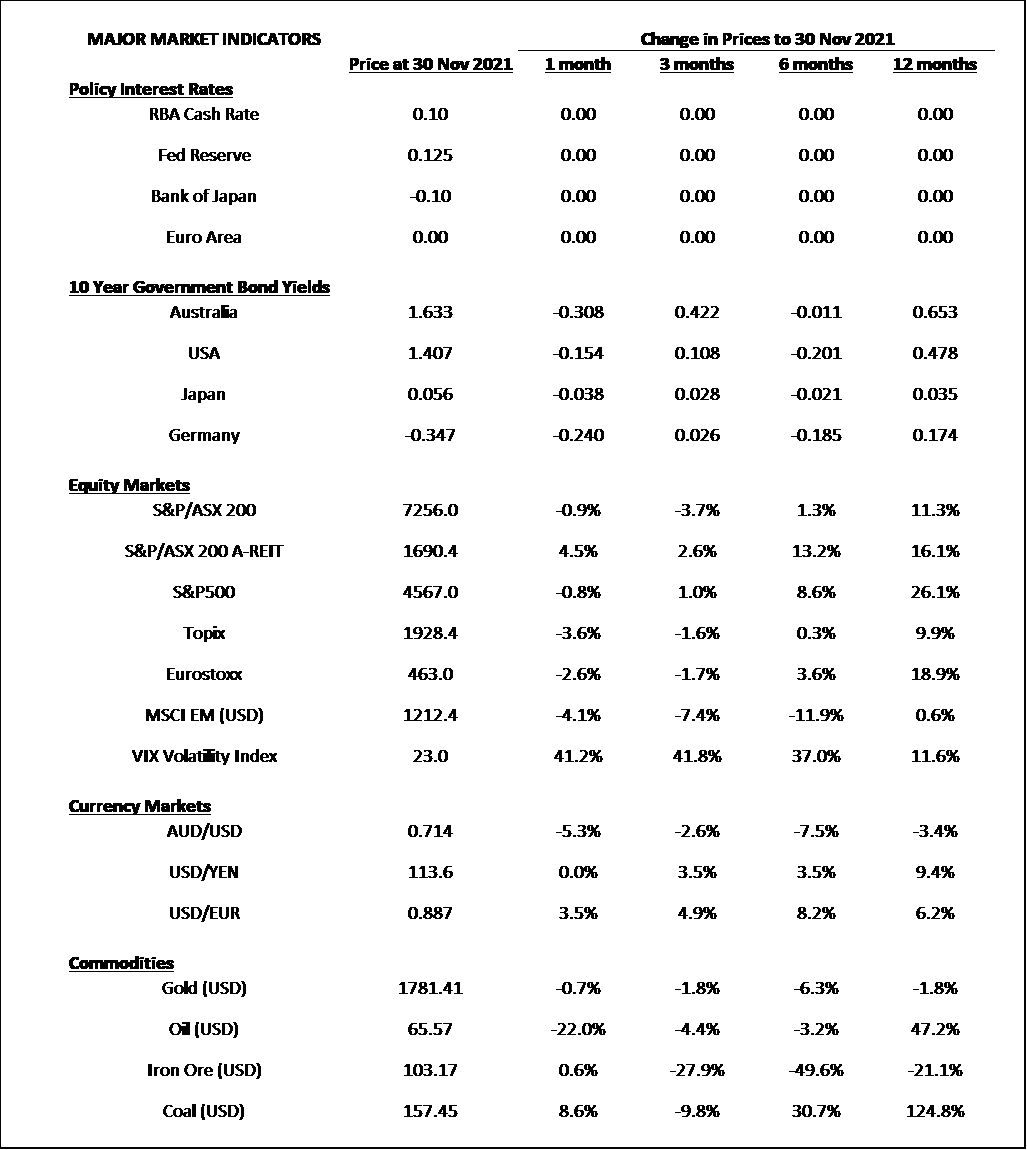

After a massive increase in bond yields in Australia and USA in October, the outlook for inflation steadied during November and

this was partially to do with concerns about Omicron potentially slowing down the global economy (until at least more is known).

- Oil prices were massively down and as one of the bigger input costs for everyone, this certainly took away some inflation strains.

- Australian 10-year bond yields closed more than 0.30% lower than at the end of October contributing to a monthly gain of over 2% for the Australian bond market.

- US 10-year bond yields were also down, although at a lower 0.15%, and contributed to a monthly gain of 0.74% for Global Bonds.

-

The emergence of Omicron also frightened sharemarkets and the Fear Index (VIX index), which measures the outlook for volatility, ended at a

value of 23 which was an increase of over 40% during November.

- This coincided with Global equity markets generally flat or down for November, although unhedged positions ended up higher by around 4%. This is because the Australian Dollar declined by more than 5% against the US Dollar and now sits around $0.71USD.

- The Australian Dollar weakness was unsurprising considering the continued slide in the price of Australia’s biggest export, Iron Ore, (around half of what it was 6 months ago) along with the previously mentioned lower bond yields. These are two of the biggest influences in the value of the Australian Dollar.

Economies

Inflation still high with mixed economic results

- Whilst inflation figures continue to be high (3% in Australia, 6% in USA), thanks to global supply chain issues, Australia’s GDP result for the September quarter showed economic decline of almost 2% in real terms. This decline was expected as NSW and Victoria were shut down for this whole period.

- The latest economic results by the largest economies have been mixed recently, including a decline of 0.8% over the quarter in Jap, increase by a strong 4.9% in both China and USA, and an increase of 3.7% in the Euro area.

Outlook

- Once again, COVID-19 has come to the fore and the testing of the effects of the Omicron variant is likely to be a leading indicator to the success or otherwise of financial markets and the major economies. Vaccination is still the key focus, but a variant that reduces the effectiveness suggests the battle will likely go for much longer and many years yet.

- With equity markets mostly pausing, and bond yields dropping, the current situation suggests that a strategy of diversification, the avoidance of large positions, and regular rebalancing continues to be the most prudent investment approach.

Major Market Indicators

Sources: Tradingview, Morningstar, Trading Economics, Reserve Bank of Australia

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL

491619