Market Snapshot: October 2023

In summary

An unchanged message … diversification not concentration

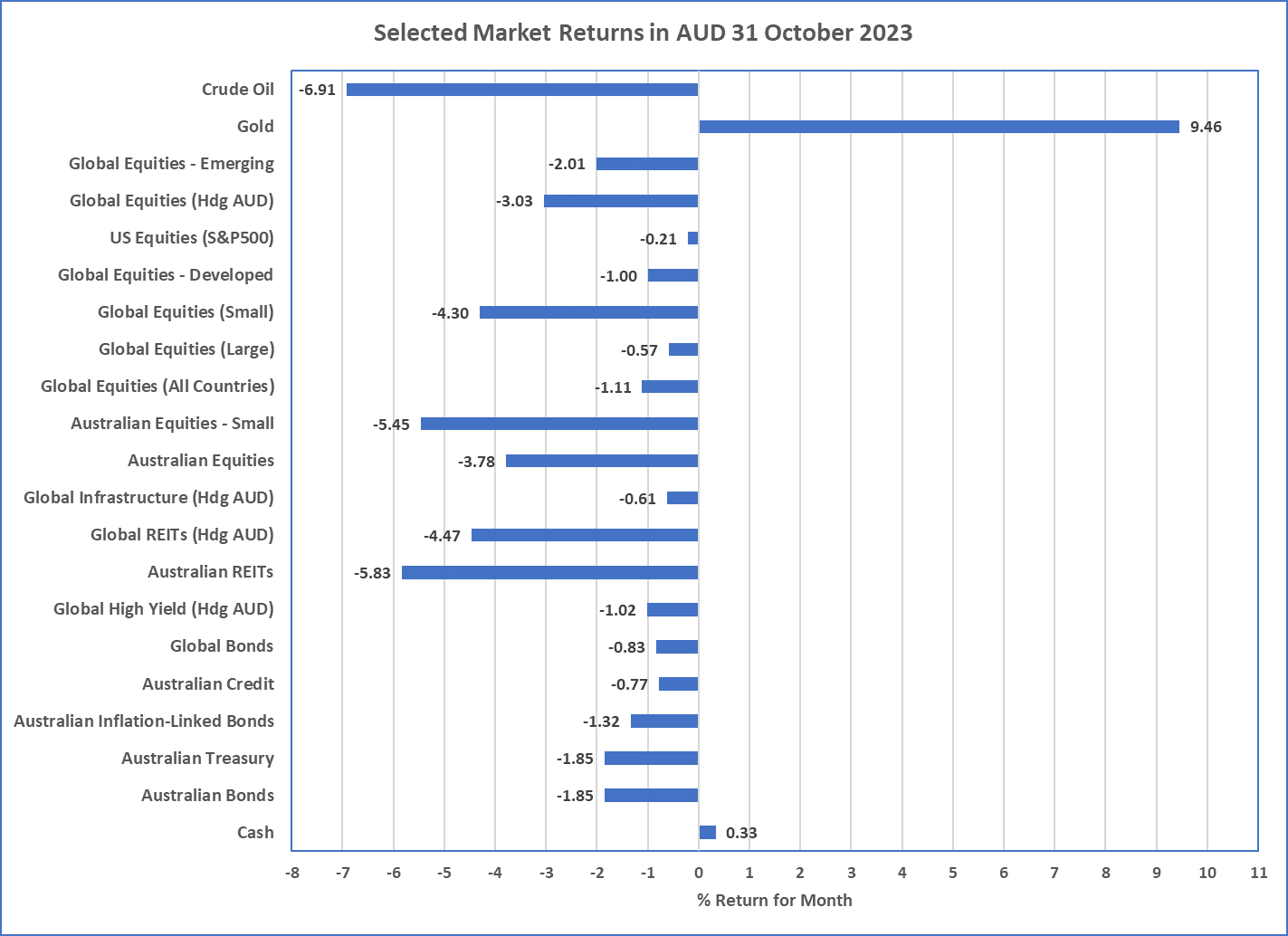

- October saw the start of another war, this time in the Middle East. This placed more pressure on Oil prices but surprisingly their price ended lower for the month. However, the occasional uncertainty hedge, that is Gold, increased in price along with the major infrastructure commodity (and Australia’s biggest export), Iron Ore. Apart from these commodities Cash was the only major asset class safe haven with everything else producing negative returns again.

- With around three months of sharemarket correction some buyers are returning with a strong start to November but with leading indicators in the USA, weakening the likelihood of US recession continues as a possibility and USA sharemarket or credit markets do not yet reflect that possibility … so caution remains.

- In Australia high inflation remains and the Reserve Bank has increased cash rates again with a chance for more in the first quarter of 2024. High rates and inflation have lead bond yields to their highest levels since 2007 making fixed interest attractive again and particularly as they may hedge the sharemarket performance in the face of a slowing US economy (if that occurs as expected).

- High valuations (particularly US shares) and slowing economies still mean it is a time for caution and portfolios continue for this with overweights to style biases such as quality and value preferred.

- Diversification over concentration, and higher than usual cash holdings appears most prudent.

Chart 1: Everything down but Cash and Gold

Source: Morningstar

What happened last month?

Markets & Economy

Yield disinversion … strangely increasing recession risks

- Another difficult month for all asset classes where the only places to hide or gain a positive return was Cash and some Commodities, such as Gold and Iron Ore. Despite the commencement of the Middle East conflict, strangely, Oil declined during October.

- From an economic perspective, the USA continued to show its resilience as lagging indicators such as unemployment remained low, and September quarter’s economic growth was reported at a surprisingly high 4.9% annualised growth rate.

- Despite the strong lagging indicators in the USA, forward looking indicators such as the government bond yield curve, and confidence indicators, continue to suggest the US economy is slowing and the most predicted recession in history still may occur … although instead of 2023 it has been pushed back to 2024 by most economists.

- The Australian economy is also showing resilience with continued low unemployment in the face of sharply rising interest rates. Inflation was reported at a high 5.4%, coinciding with another high services inflation result (6.3%), and this gave the Reserve Bank another opportunity to raise rates which it did on Melbourne Cup Day (7 Nov).

- The higher for longer inflation story continues and this continues to place upward pressure on interest rates and bond yields and in turn presents increased recession risks. This message has been consistent for some months and whilst equity markets were strong until mid-July, recent months have seen a significant sharemarket volatility which is likely to continue as valuations come under pressure in the face of slowing economies.

Outlook

More volatility but buying opportunities are coming

- The message remains largely unchanged which is that continuation of this overdue sharemarket volatility is more than likely. That said, this volatility will create opportunities as valuations begin to normalise and align with more realistic growth potential.

- It is worth saying, that despite the bond market’s horrendous performance over the last couple of years, their outlook is the best it has been for some time … bond market volatility is likely, but it’s role as a hedge to economic slowdown looks more attractive.

- From a sharemarket valuation perspective, investment markets at greatest risk continue to be the growth heavy US Tech market and higher yielding US corporate bond market. As mentioned in the past, whilst high yield spreads are tight (and therefore expensive), one positive is the high energy prices are supportive as the energy sector is a large proportion of the US High Yield market.

- All of that said, Cash remains king for now given this higher for longer inflation theme and the continued upward pressure on rates.

- Investing with styles that favour value, quality (whether bonds or equities) continues to be appropriate along with the avoidance of concentrated bets in favour of diversification.

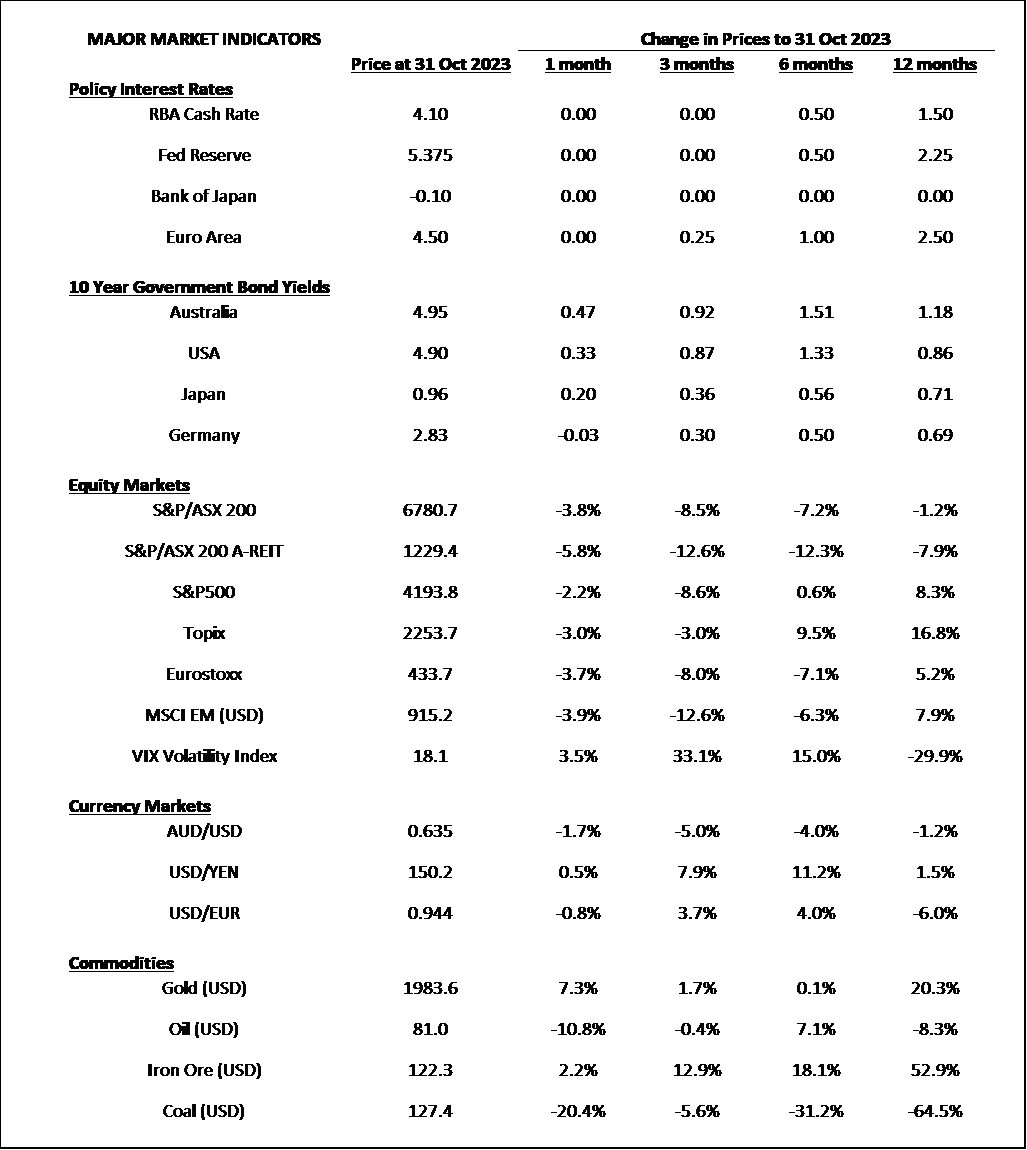

Major Market Indicators

Sources: Tradingview, Morningstar, Trading Economics, Reserve Bank of Australia

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL 491619