Market Snapshot: September 2025

Summary

A quiet month with a repetitive message

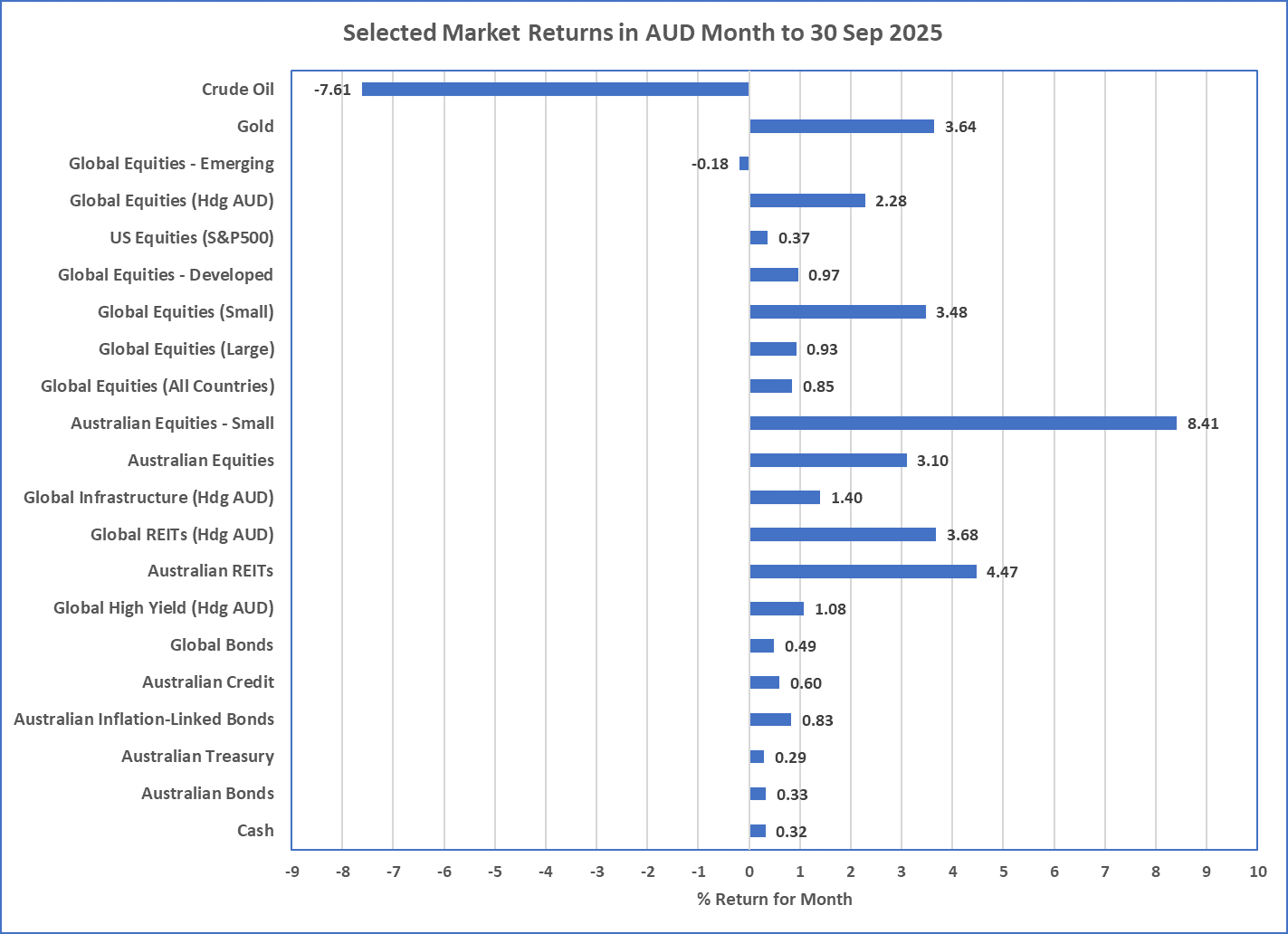

- REITs and Small Companies were the standout performers during September, but all major asset classes produced positive returns except emerging markets which were flat.

- The only cash rate move was a 25bps rate reduction from the USA’s Federal Reserve, but looking ahead a weaker looking economy combined with higher inflation creates ongoing uncertainty. Bond yields were relatively steady around the world, and this resulted in small returns from all fixed interest markets, whether locally or globally.

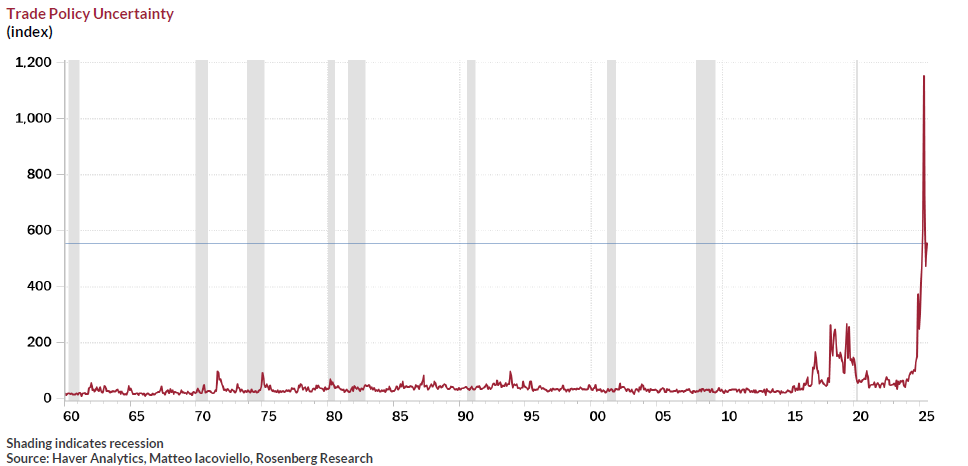

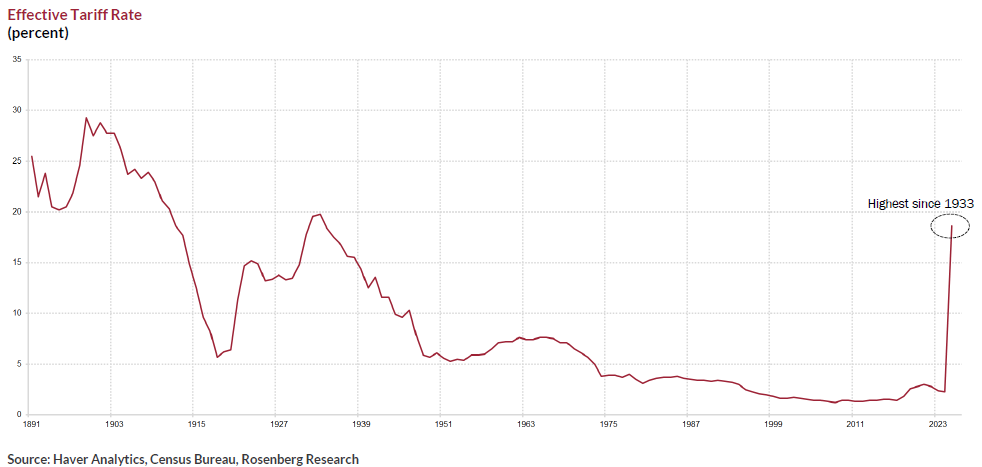

- Looking ahead the main short-term factor that may change market volatility is likely economic data in the USA from September quarter results. This will be the first full quarter that include tariffs announced (and sometimes removed) since “Liberation Day” in April. Otherwise, nothing has changed in terms of valuations as USA sharemarket valuations continue amongst the highest this century. This is influencing a long-term bearish outlook for many investors.

- Our core investment message today is to maintain diversification, focus on the long term, and regularly rebalance. Major risks continue to lie with expensive sharemarkets (irrespective of artificial intelligence confidence and the prospect of illegal tariffs), including large companies of the USA, and we continue to favour quality (i.e. good profitability) and value (i.e. “cheap”) styles for long term investments in shares. Quality bonds are preferred as higher yielding below-investment grade bonds provide a historically low premium.

Chart 1 … REITs and Small Caps win September

Source: Morningstar

What happened last month?

Markets & Economy … relatively uneventful

- As far as markets and economic data is concerned, September was a relatively benign month. All major asset classes increased in value, except Emerging markets which ended flat, there were no major economic surprises, so the tech stock and risky asset momentum continued.

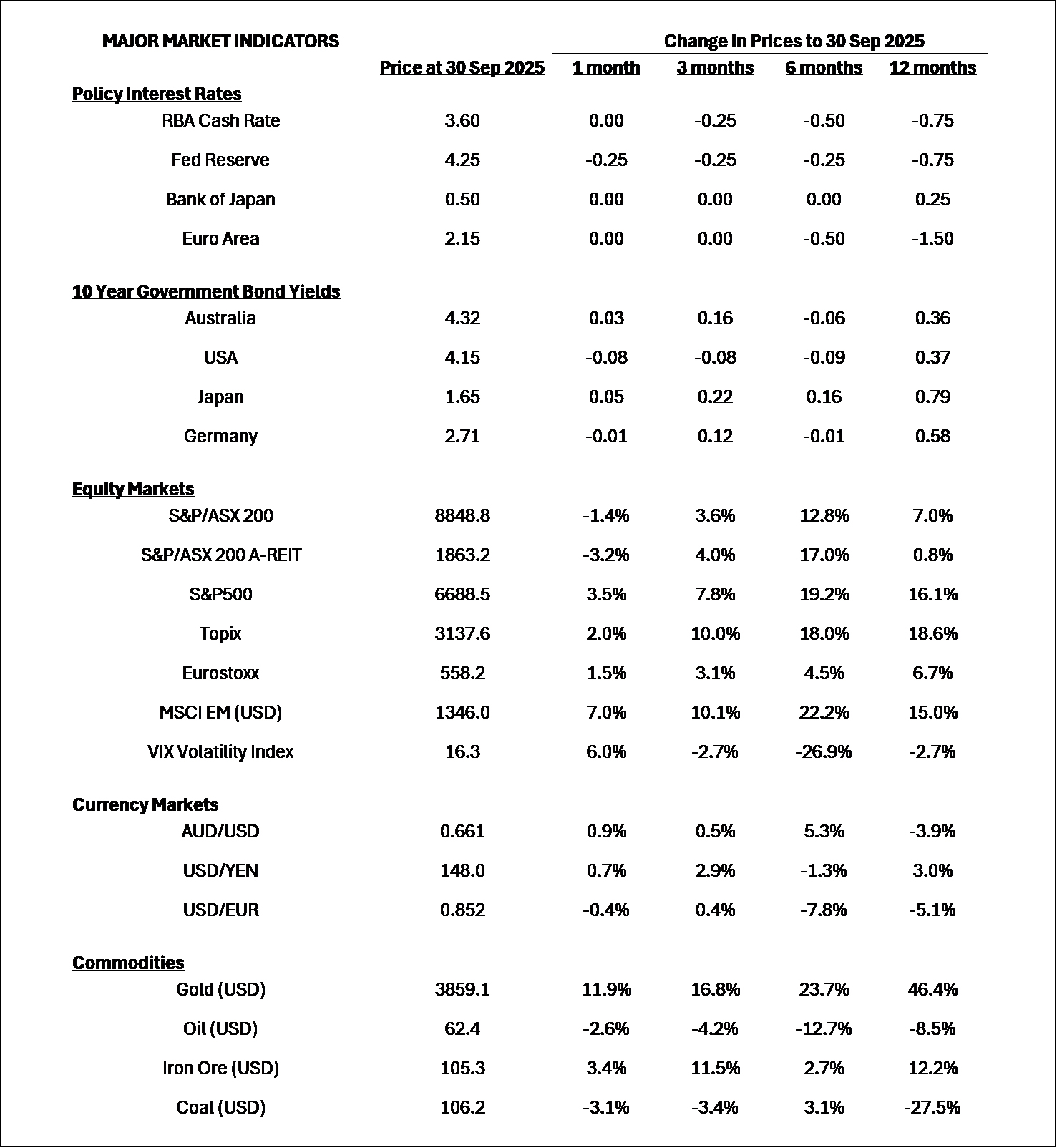

- Amongst central banks, most kept cash rates unchanged although the Federal Reserve reduced by 25bps. This could have been more as the tariffs place downward pressure on the economy, but at the same time inflation is creeping up (US inflation is 2.9%) meaning they could have kept the rate unchanged. So, the Fed chose to take the middle road with a small decrease.

- In Australia the Reserve Bank kept cash rates at 3.6% following higher than expected inflation and steady and low unemployment (4.2%). As a result, markets have reduced the probability of future rate reductions but still price in 1 possible reduction over the next 6 months.

- Bond yields were relatively steady around the world during September, although Japan’s have continued their slow upward creep. Japanese interest rates continue to be amongst the lowest in the world but their latest inflation result (2.7%) is amongst the highest across the developed world.

- The fourth quarter of 2025 should prove the most telling in terms of economic growth around the world as this will be the first full quarter which includes many of the impacts of the USA-imposed tariffs.

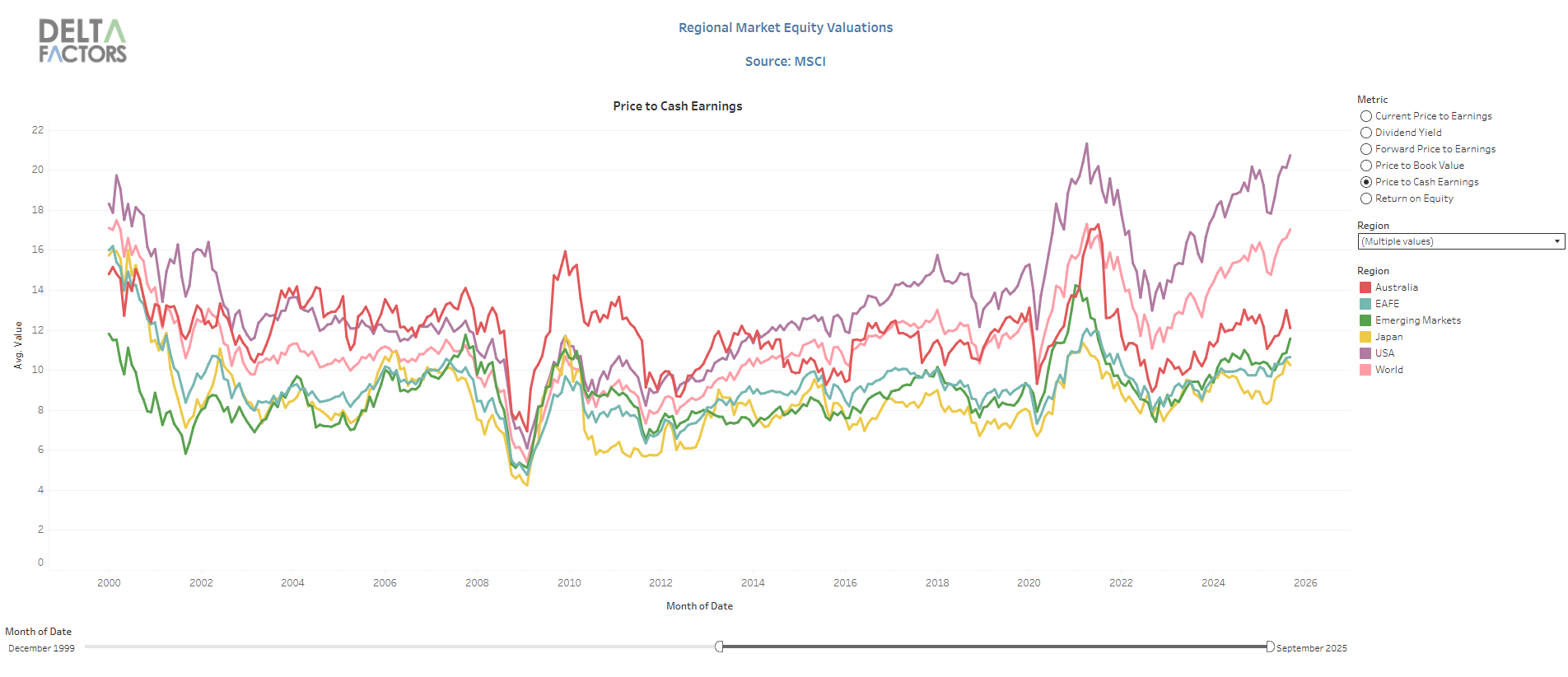

Outlook …US Sharemarket valuations remain the concern

- This paragraph is intentionally a repeat of last month’s because very little has changed at the macro level. Artificial Intelligence continues its boom, and valuations continue to be stretched.

- Strong sharemarkets have kept the US Sharemarket at high valuations. As reported last month, they are heading towards the pre-correction 2021 levels and are near the highest valuations this century. Other markets, including Australia appear fully valued, although Europe, Japan and Emerging Markets appear somewhat fairly valued.

- Whilst US employment data has shown weakness, the full effects of tariffs will only start being reports as September is the first full quarter since tariffs were originally in place. Artificial Intelligence capital expenditure continues as the growth engine for now.

- Inflation in Australia reduced to 2.1% in the June quarter and current pricing suggests the Reserve Bank of Australia will probably only produce one more 25bps rate cut over the next 6 months as economic data has been stronger than previously expected. With the USA starting to produce weaker data, like unemployment, further rate cuts may occur, although the caveat is around high inflationary effects expected from tariffs.

- Overall, the general portfolio preferences are unchanged and centres on diversification. Volatile markets are likely to continue, and diversification continues to be essential in this environment, whether shares, bonds, real assets, as well as across regions and broader asset class levels. Over the long-term, we believe valuation matters and this continues to be another central theme for investment today.

Major Market Indicators

Sources: Morningstar, Trading Economics, Reserve Bank of Australia

Source: Morningstar

Source: Delta Research and Advisory, MSCI

McConachie Stedman Financial Planning Pty Ltd is a Corporate Authorised Representative of MCS Financial Planning Pty Ltd | ABN 11 677 710

600 | AFSL 560040

General Advice Warning

The information provided in this article is for general information purposes only and is not intended to and does not constitute formal

taxation, financial or accounting advice. McConachie Stedman does not give any guarantee, warranty or make any representation that the

information is fit for a particular purpose. As such, you should not make any investment or other financial decision in reliance upon the

information set out in this correspondence and should seek professional advice on the financial, legal and taxation implications before

making any such decisions